Dubai Hospitality Market Performance 2025

Hospitality Market Overview

Dubai’s tourism sector has grown steadily over the past few years, benefiting from world-class infrastructure, a safe and diversified environment, and a strong calendar of events and cultural festivals. The market continued to perform strongly in 2025, supported by strong air connectivity, rising international visitation, and resilient hotel performance. Passenger traffic at Dubai’s airports reached 95.2 million up by 3.1% compared to 2024, with international visitors climbing to 19.6 million, reinforcing the Emirate’s position as a leading hub for both leisure and business travel. Demand growth remains broad-based, supported by a diversified mix of source markets and an expanding ecosystem of events and experiences, while premium hotel openings have further enhanced Dubai’s appeal to high-value international travellers.

On the supply side, the market has transitioned into a more balanced and demand-aligned growth phase. Hotel inventory expanded modestly with total room inventory reaching 158,700 in 2025, allowing strong absorption and maintaining healthy occupancy levels of 81% citywide alongside 8.7% Average Daily Rate (ADR) growth. The existing stock is increasingly weighted toward Upscale, Upper-Upscale, and Luxury segments, reflecting Dubai’s premium positioning, while future supply is similarly concentrated in higher-end offerings.

Looking ahead, the outlook for Dubai’s hospitality market presents a more nuanced picture. Whilst geopolitical tensions in the region introduce near-term uncertainty for travel patterns and visitor flows, Dubai’s core fundamentals remain robust. The Emirate benefits from both a diversified global visitor base spanning Europe, North America, Asia, and beyond, as well as steady domestic demand, supporting a degree of stability amid potential headwinds. Strategic Government initiatives, continued investment in transport and urban infrastructure, and a strong pipeline of events are expected to support the sector. Combined with proven crisis recovery capabilities and ongoing infrastructure expansion, the Emirate is expected to maintain its position as one of the world’s most resilient, competitive, and diversified tourism destinations.

Market Snapshot for 2025

- International visitors: 19.6 million (+4.6% Y-on-Y)

- Average Daily Rate (ADR): AED 746.4 (+8.7% Y-on-Y)

- Occupancy Rates: 81% (+3.8% Y-on-Y)

- Estimated Upcoming Hotel Supply (2026)

- Hotels: 21

- Rooms: ~4,600

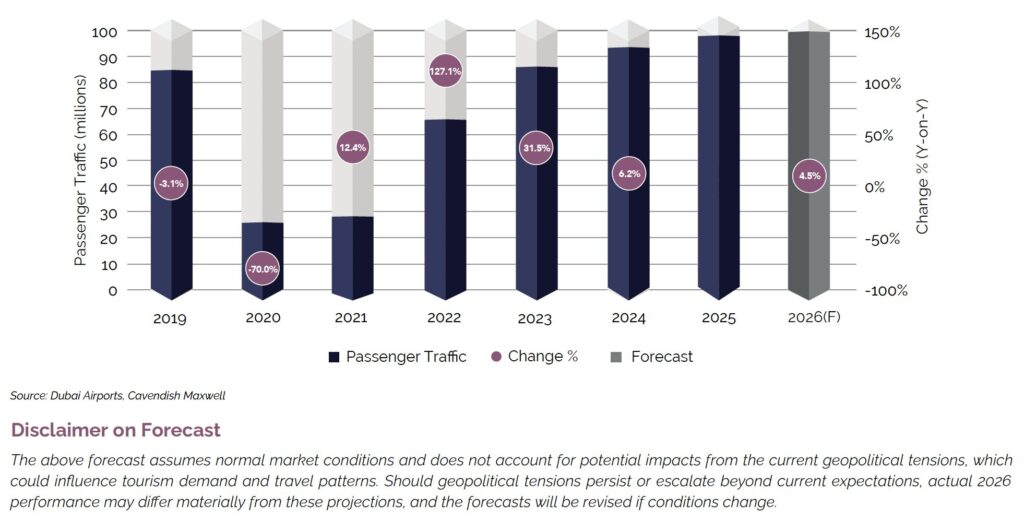

Dubai Airport Passenger Traffic

In 2025, Dubai International (DXB) recorded a historic 95.2 million passengers, a 3.1% year-on-year increase, marking the highest annual international passenger traffic ever recorded by any airport and putting the Emirate within striking distance of the 100-million milestone. The year closed on a particularly strong note, with Q4 2025 emerging as the busiest quarter in DXB’s history, handling 25.1 million passengers, up 5.9% compared to the same period in 2024. Total flight movements climbed to 454,800 across the year, a 3.3% rise, with the final quarter contributing 118,000 movements.

On the destinations front, London retained its position as DXB’s busiest city destination, drawing 3.9 million passengers, followed closely by Riyadh at 3 million. Mumbai, Jeddah, and New Delhi rounded out the top five. By year-end, DXB’s network had expanded to 291 destinations across 110 countries, served by 108 international airlines, further cementing its standing as the world’s most connected hub.

While DXB continued to handle the bulk of traffic, Al Maktoum International Airport (DWC) emerged as a critical piece of Dubai’s long-term aviation strategy. Passenger traffic at DWC is estimated to have reached between 1.3 and 1.5 million in 2025, up from 1.1 million in 2024, reflecting its role as a strategic relief airport for selected regional markets, particularly Saudi Arabia.

Passenger Traffic – Dubai International Airport (DXB)

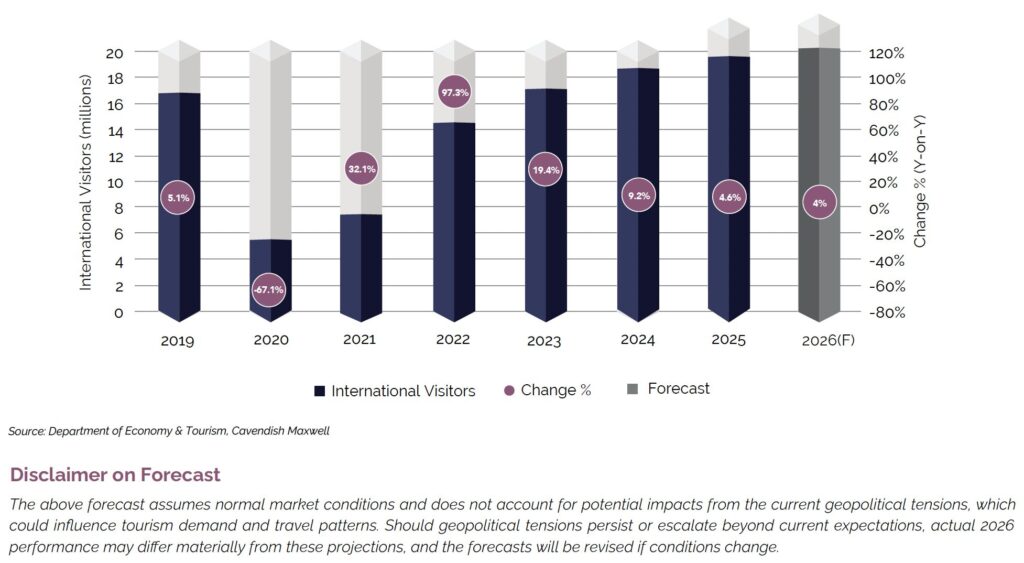

International Visitors

Dubai’s tourism sector reached new heights in 2025, welcoming 19.6 million international visitors, a steady 4.6% increase from 2024. This growth was supported by Dubai’s increasingly diversified offerings, including an expanded event calendar, a growing portfolio of luxury and ultra-luxury hotels, adventure experiences, world-renowned shopping festivals, a strong safety profile, and a vibrant culinary scene. Collectively, these factors have driven a meaningful shift in travel behaviour, moving beyond traditional sightseeing towards high-impact experiential travel.

Looking ahead, the Dubai Department of Economy and Tourism (DET) plans to further accelerate visitor growth in 2026 through expanded marketing campaigns, strengthened airline and hotel partnerships, and initiatives spanning cultural festivals, adventure experiences, business-conference incentives, and curated luxury packages. As a result, international arrivals are projected to reach 20.4 million in 2026. These efforts are also firmly aligned with Dubai’s long-term ambition under the D33 Economic Agenda to become one of the world’s top three destinations for both business and leisure travel by 2033.

Total International Visitors

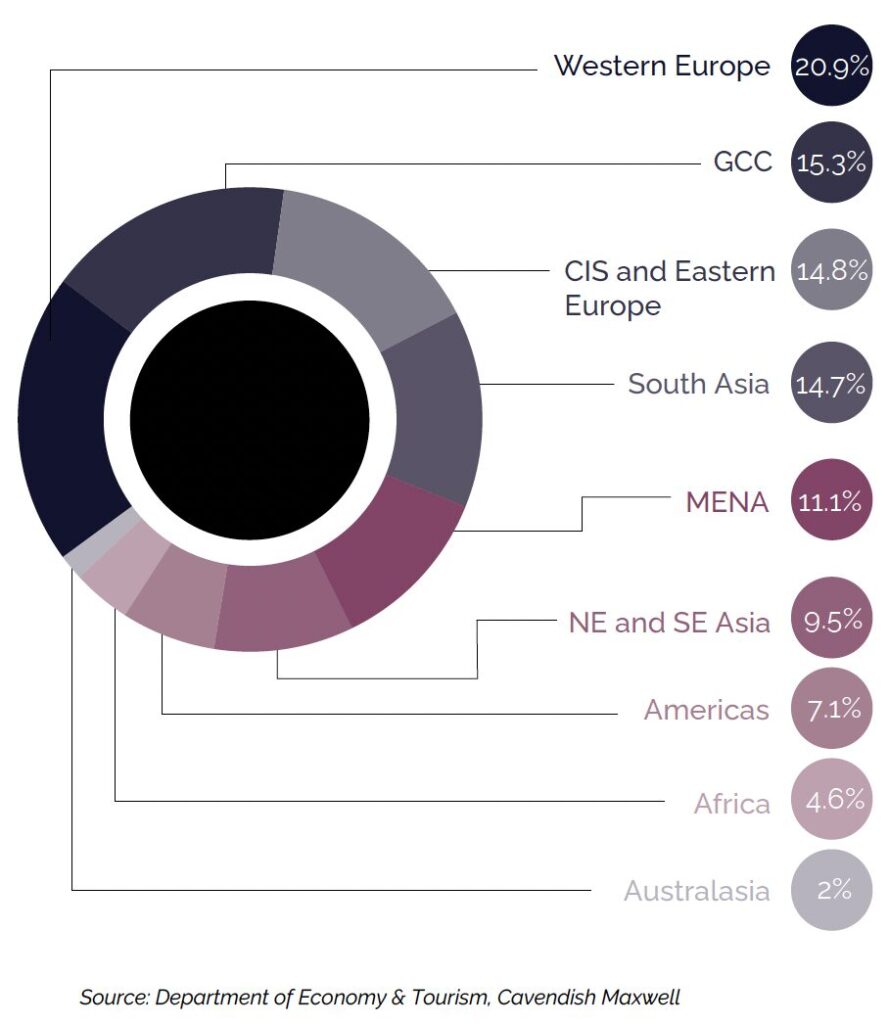

International Visitors: By Source Market

Dubai’s international visitor profile in 2025 reflected a well-balanced and globally diversified demand base. Western Europe remained the largest source region, accounting for 20.9% of total arrivals, followed by the GCC (15.3%), CIS & Eastern Europe (14.8%), and South Asia (14.7%). While South Asia recorded a 7.9% decline compared to 2024, Western Europe grew by 9.7%, the GCC by 9.3%, and CIS & Eastern Europe by 10.1%. The remaining arrivals were distributed across Middle East and North Africa (11.1%), North and Southeast Asia (9.5%), the Americas (7.1%), Africa (4.6%), and Australasia (2%).

Tourism flows from Europe were further supported by enhancements in connectivity in 2025, including the restoration of Emirates’ A380 services on the London–Dubai route, the resumption of five-weekly Vienna–Dubai flights, and increased capacity on other key European routes. Network expansion across the GCC and Asian markets also contributed to broader regional accessibility, strengthening Dubai’s appeal for both short-haul and long-haul travellers.

This broad mix of international visitors reinforces Dubai’s global appeal while providing a resilient foundation for the tourism sector, limiting reliance on any single source market. A combination of factors such as travel accessibility, targeted marketing, favourable exchange rates, improved connectivity, and visa facilitation supported higher arrivals. These dynamics influenced not only overall visitor numbers but also the segments of Dubai’s tourism and hospitality industry that benefited the most, from luxury retail and hotels to short-stay and family-oriented offerings.

Dubai Tourism Distribution By Region (January – December 2025)

Dubai’s hospitality market performed strongly in 2025, with international arrivals approaching 20 million and hotel occupancy exceeding 81%, supported by solid demand fundamentals, measured supply growth, and the city’s unrivalled global connectivity.

Ferras Hafez

Associate Director, Commercial Valuation

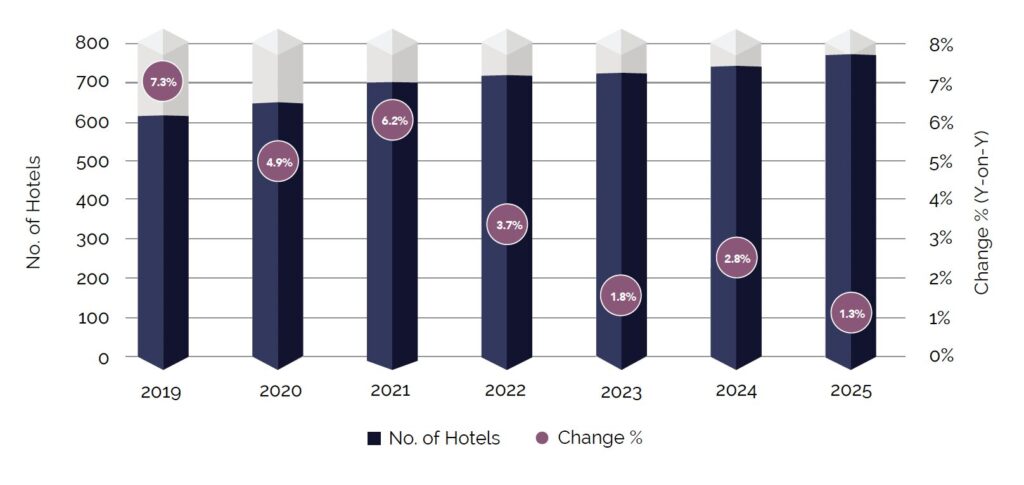

Current Supply

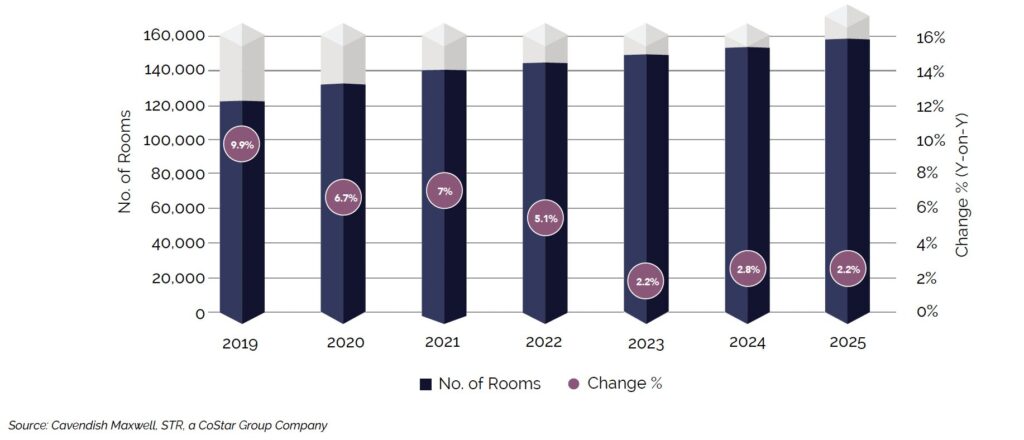

According to the latest figures, by December 2025, the Emirate hosted around 770 hospitality establishments, offering approximately 158,700 rooms.

The supply side of the picture

The hospitality industry has been keeping up with tourism levels in Dubai, adjusting supply to meet demand.

Our insights reveal that:

Existing Hospitality Supply

In 2025, amid stronger growth in visitor numbers, Dubai’s hospitality supply expanded at a measured pace. The number of hotels increased from around 760 to 770, representing a 1.3% year-on-year rise, while total room inventory grew by 2.2% year-on-year to approximately 158,700 rooms. As visitor growth outpaced new supply additions, operating conditions across the hospitality market remained supportive, particularly in terms of occupancy performance.

Hospitality Building Supply – 2019 to 2025

Hospitality Room Supply – 2019 to 2025

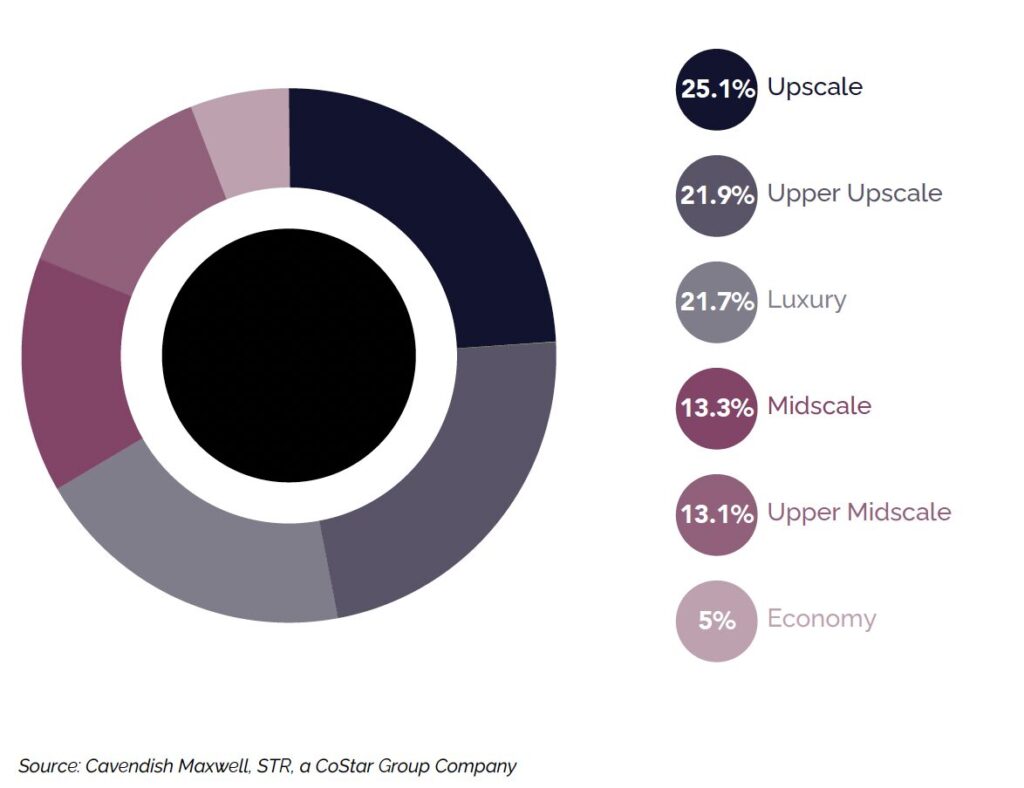

Current Hospitality Room Inventory: By Classification

Dubai’s hospitality room inventory by the end of 2025 was concentrated in the luxury and upscale segments, reflecting the Emirate’s positioning as a premium global destination. Upscale hotels accounted for the largest share of supply at 25.1%, followed by the Upper Upscale and Luxury segments at 21.9% and 21.7%, respectively, together representing nearly half of the total room inventory. The Midscale and Upper Midscale segment accounted for 13.3% and 13.1%, respectively, supporting value-driven and business-oriented demand, while the Economy segment remained limited at 5%.

Hotel openings during 2025 were largely concentrated in the luxury segment, with notable additions including Ciel Dubai Marina, Jumeirah Marsa Al Arab and Mandarin Oriental Downtown. Upper-Upscale supply also expanded through new additions such as Vida Dubai Mall and Hotel Local Dubai Jumeirah Village Triangle, catering to both leisure and business travellers.

Current Hospitality Room Inventory by Classification – As of 2025

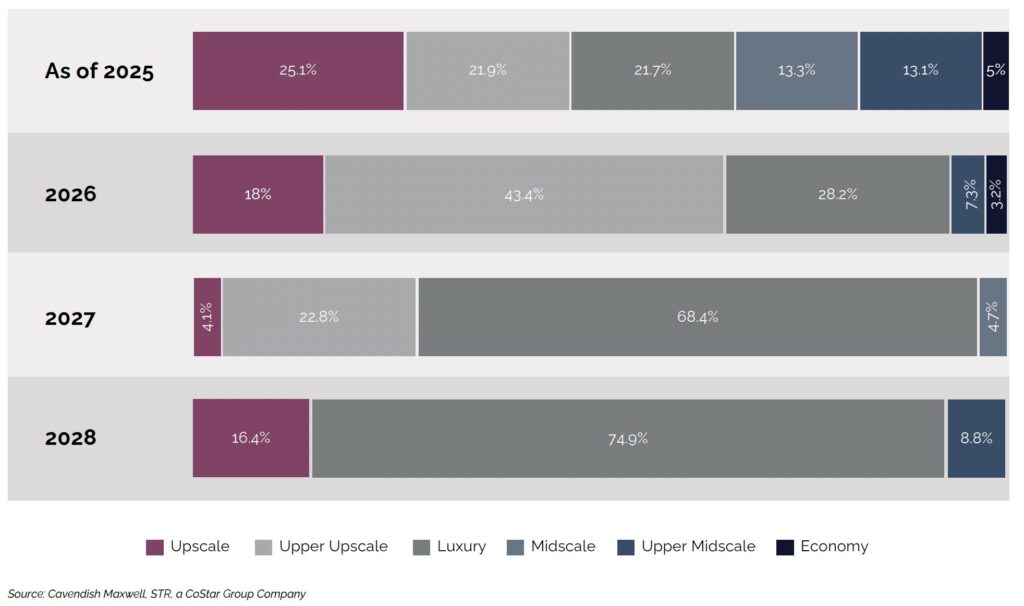

Future Supply

Looking ahead, around 41 new hotels, totalling approximately 9,300 keys, are scheduled for delivery by 2028, with most expected to open in 2026. Nevertheless, actual completions are likely to be lower, as observed in 2025, keeping demand ahead of supply in near term.

In terms of classification, Dubai’s future hotel supply pipeline points to a clear shift towards higher-end segments. While the existing inventory in 2025 remained relatively balanced across the Upscale, Upper-Upscale and Luxury categories, the pipeline through to 2028 is notably skewed towards the Luxury (49.8%) and Upper-Upscale (28.6%) segments, with only limited additions in the midscale and economy categories. This trend is expected to become even more pronounced in 2027, when luxury hotels are projected to account for around 68.4% of the upcoming supply.

The growing concentration of luxury developments reflects Dubai’s broader positioning as a global premium tourism destination, supported by strong demand from high-spending international visitors and the Emirate’s increasing focus on experiential and wellness-led hospitality concepts. The coming years are also expected to see the debut of several high-profile developments, including the Baccarat Hotel & Residences Dubai and the wellness-focused Six Senses The Palm Dubai in 2026. In addition, projects such as Floating Venice Dubai and the Kempinski Floating Palace Dubai are set to further expand the Emirate’s on-the-water hospitality offering.

Hospitality Room Inventory by Classification – Upcoming Supply

Market Performance

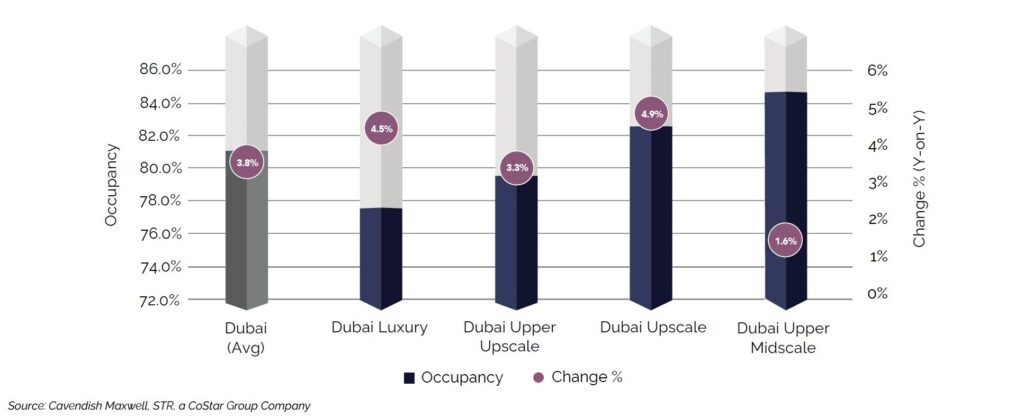

Occupancy

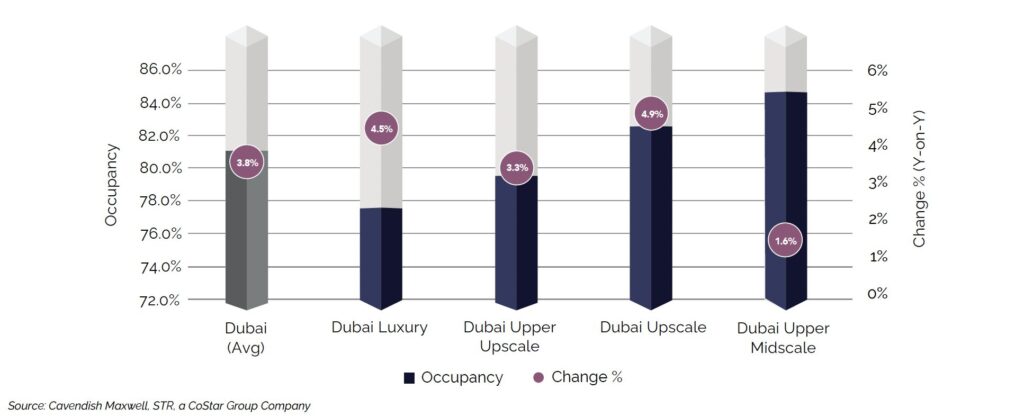

Dubai’s hospitality sector recorded strong performance in 2025, with city-wide occupancy reaching 81%, representing a 3.8% increase compared to 2024. Growth was observed across all segments, most notably in the Upscale segment, which recorded the highest increase at 4.9%, followed closely by the Luxury segment at 4.5%.

The Upper Midscale segment had the highest overall occupancy at 84.4% but saw modest growth at 1.6%; this segment remained particularly popular among value-conscious business travellers and mid-market families who prioritised quality, accessibility and location over luxury amenities. Overall, the increase in occupancy across segments highlighted the continued strength of visitor demand in Dubai, which remained sufficient to absorb new room supply entering the market.

Occupancy by Classification – 2025

Average Daily Rate (ADR)

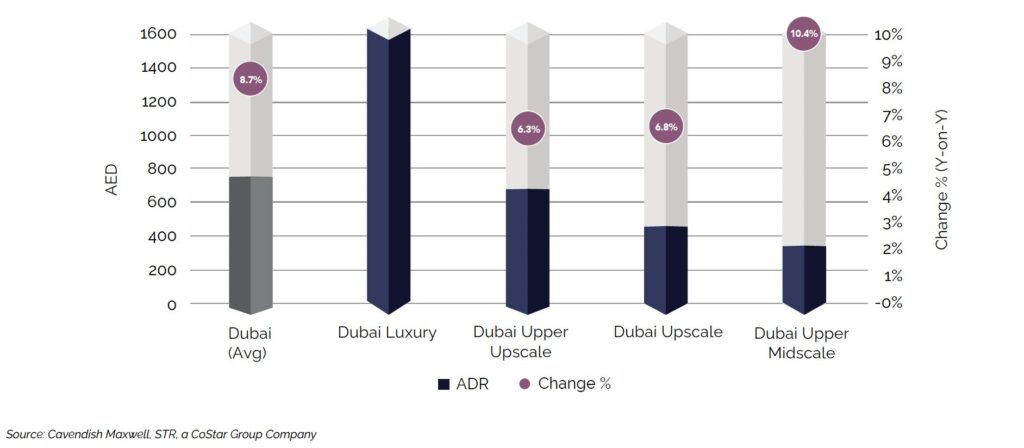

Dubai’s hospitality sector saw strong growth in Average Daily Rates (ADR) in 2025, supported by high demand and effective pricing strategies. This allowed hotels to raise rates without risking unoccupied rooms. The city-wide ADR reached AED 746, an increase of 8.7% compared to 2024. All segments recorded positive growth, with the Upper Midscale segment posting the highest increase of 10.4%, followed by Luxury (7.6%), Upscale (6.8%), and Upper Upscale (6.3%) segments.

The Luxury and Upper Upscale segments benefited from strong demand from high-spending international visitors, while the Upper Midscale segment was supported by steady demand from business travellers and mid-market families. The Upscale segment achieved solid growth through a combination of strong occupancy gains and rate increases, positioning it as a key revenue driver for the market.

Overall, the combination of strong international and domestic demand, limited supply growth, and rate management strategies by hotels contributed to robust ADR performance across Dubai’s hospitality market in 2025.

Average Daily Rate by Classification – 2025

Hospitality Market Forecast

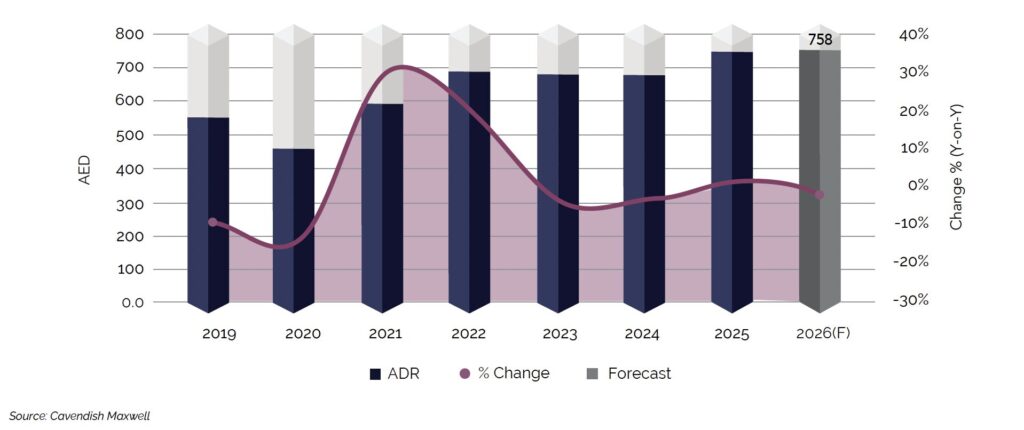

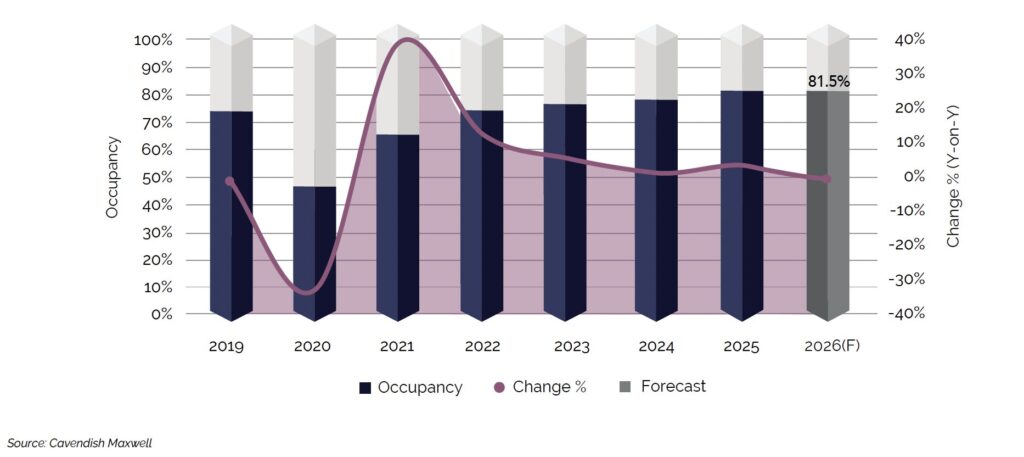

Dubai’s hospitality market’s upward momentum is expected to continue into 2026, supported by steady visitor demand. Average daily rates (ADR) are forecast to reach AED 758, up 1.6%, with occupancy projected at 81.5%. Around 4,600 rooms are scheduled for delivery by year-end, primarily in the Upper Upscale and Luxury segments, which posted strong growth in 2025. While actual completions may fall short, full delivery could temporarily ease occupancy pressures in these segments. Overall, baseline tourism demand is expected to support the market throughout 2026, maintaining stable operating conditions.

Average Daily Rate (ADR) – Historic and Forecast

Occupancy – Historic and Forecast

Disclaimer on Forecast

The above forecast assumes normal market conditions and does not account for potential impacts from the current geopolitical tensions, which could influence tourism demand and travel patterns. Should geopolitical tensions persist or escalate beyond current expectations, actual 2026 performance may differ materially from these projections, and the forecasts will be revised if conditions change.

Hospitality Market Performance – Other Emirates

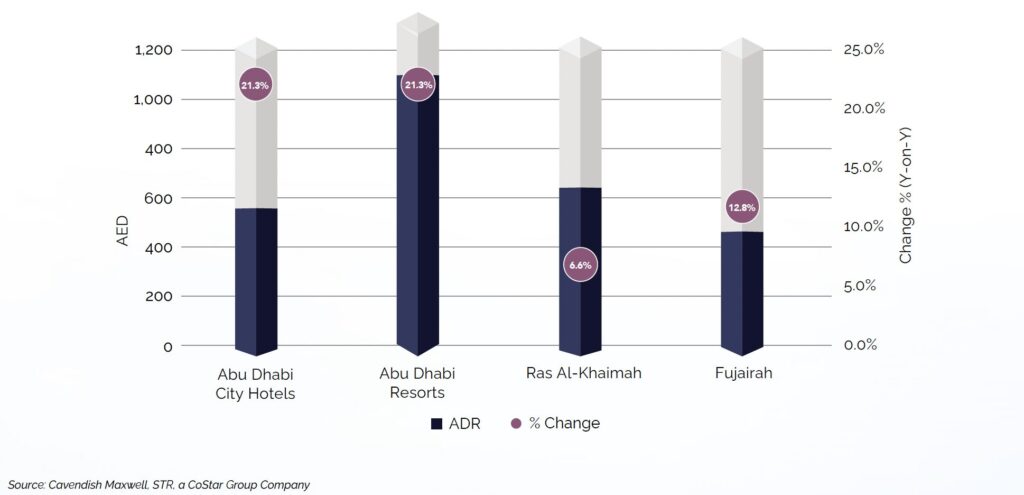

Hospitality performance across the other Emirates remained strong in 2025, supported by robust occupancy levels and ADR growth. Abu Dhabi City hotels led the market with an occupancy rate of 82.8% and ADR growth of 21.3%, while Abu Dhabi resorts achieved 78.6% occupancy with ADR reaching AED 1,098, also up 21.3% year-on-year. This growth reflects Abu Dhabi’s evolution into a premier cultural destination, anchored by world-renowned museums and interactive galleries concentrated in the Saadiyat Cultural District, including the Zayed National Museum, the Natural History Museum, and the iconic Louvre Abu Dhabi.

Beyond Abu Dhabi, Ras Al Khaimah also demonstrated strong hospitality performance in 2025, with occupancy reaching 75%, up 4.6% year-on-year, while ADR increased to AED 618, up 6.6%. This performance was driven by the Emirate’s record tourism results, welcoming 1.35 million overnight visitors, a 6% increase compared with the previous year, while tourism revenues rose by 12%. The expansion was further supported by expanded air connectivity, signature events such as the RAK Half Marathon, new hotel supply including Rove Al Marjan Island and SO/ Ras Al Khaimah, and major luxury brand announcements from Janu and Giorgio Armani, which strengthened the destination’s lifestyle and leisure positioning.

Fujairah maintained stable occupancy at 74.9% in 2025, while ADR increased to AED 433, reflecting growth of 12.8%. The Emirate continues to attract weekend and domestic leisure demand, supported by its natural landscape combining mountain terrain and coastline. Over the next three to five years, Fujairah plans to expand its adventure tourism offering through infrastructure upgrades, including specialised trails and eco lodges. Planned initiatives include the expansion of Fujairah Adventure Park, the introduction of geo tourism experiences, and the establishment of a training centre to certify local guides in line with international safety and sustainability standards.

Occupancy by Classification – 2025

Average Daily Rate by Emirates – 2025

2026 Hospitality Market Outlook

Dubai’s tourism and hospitality sector delivered strong performance in 2025, driven by robust domestic and international visitor demand, strategic air connectivity, and an expanding calendar of global events. Passenger traffic reached 95.2 million while international arrivals climbed to 19.6 million, cementing the Emirate’s status as a leading global tourism hub. This momentum translated directly into hotel sector strength, with occupancy rates and average daily rates both trending upward throughout the year.

The 2026 outlook presents a more nuanced picture. While geopolitical tensions in the region introduce near-term uncertainty for travel patterns and visitor flows, Dubai’s core fundamentals remain robust. The Emirate benefits from both a diversified global visitor base spanning Europe, North America, Asia, and beyond, as well as steady domestic demand, supporting a degree of stability amid potential headwinds. Combined with proven crisis recovery capabilities, ongoing infrastructure expansion, and a strong events pipeline anchoring demand, these structural factors position the sector for continued growth despite cyclical headwinds.

Historically, Dubai’s tourism market has demonstrated superior resilience during periods of uncertainty, recovering quickly as conditions ease. The city’s competitive advantages extend beyond its global visitor diversity and connectivity, anchored by continuous investment in physical infrastructure and experiential attractions. As these structural supports remain in place, the sector is expected to navigate near-term volatility while maintaining its longer-term growth trajectory.