Oman Hospitality Market Performance 2025

Executive Summary with Key Trends

Oman’s hospitality sector delivered a strong performance in 2025, supported by continued growth in tourism demand and improving connectivity. Airport traffic reached 14.9 million passengers, up 2.8% year-on-year, reflecting steady recovery momentum and enhanced route networks. This translated into solid hotel performance, with the 3–5-star segment welcoming approximately 2.4 million guests, a 10.8% increase compared to 2024, supported by both domestic and international segments, contributing to greater demand diversification.

As a result, operational performance strengthened across the sector, with total hotel revenues rising to OMR 297.3 million, up 22.2% year-on-year and the highest level in recent years. This growth was primarily driven by higher occupancy, which increased to an average of 56.7%, indicating improved utilisation of available room stock. Whilst average room rates increased by 4.7% in 2025 to OMR 48.6, performance was notably stronger during the winter months, reflecting the market’s ability to capitalise on peak seasonal demand. Overall, the sector has moved beyond recovery, with growth increasingly supported by structural demand drivers and gradual improvement in shoulder-season performance.

Looking ahead, the market enters 2026 on a solid footing, supported by a measured pipeline of new supply. Approximately 2,400 rooms are expected to be delivered in 2026, followed by a further 900 rooms in 2027. If demand growth continues in line with new supply additions, the market is expected to absorb additional capacity while maintaining healthy performance. While regional geopolitical developments may pose near-term uncertainties, Oman’s strong destination fundamentals, supported by proactive tourism initiatives and ongoing infrastructure investment, are expected to sustain its growth trajectory.

Tourism Sector Overview and Performance

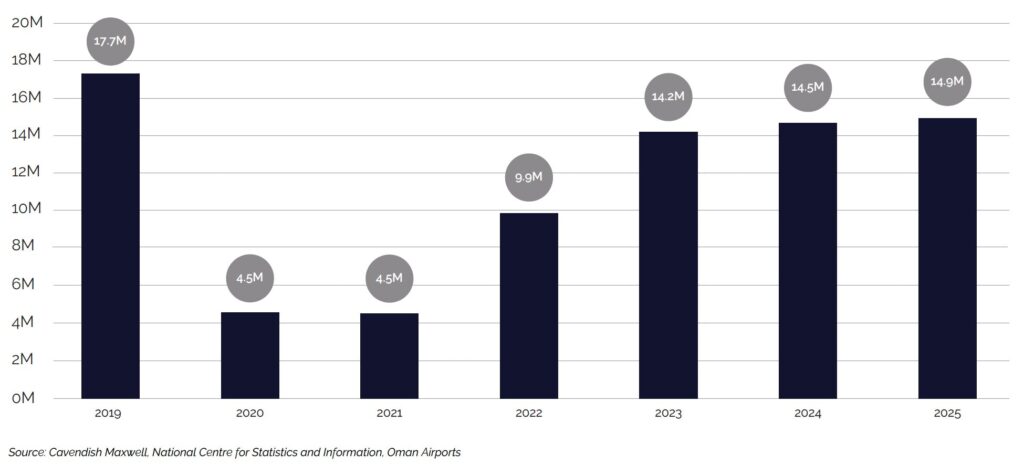

Airport Passenger Volume Trends

Oman’s airport network handled 14.9 million passengers in 2025, up 2.8% from 14.5 million in 2024, extending the recovery that began in 2022. Traffic remained steady throughout the year, with August recording the highest monthly volume at approximately 1.7 million passengers during Salalah’s Khareef season. The growth reflected improving route connectivity and rising appeal of Oman as a travel destination.

Airport Passenger Volume (in Millions)

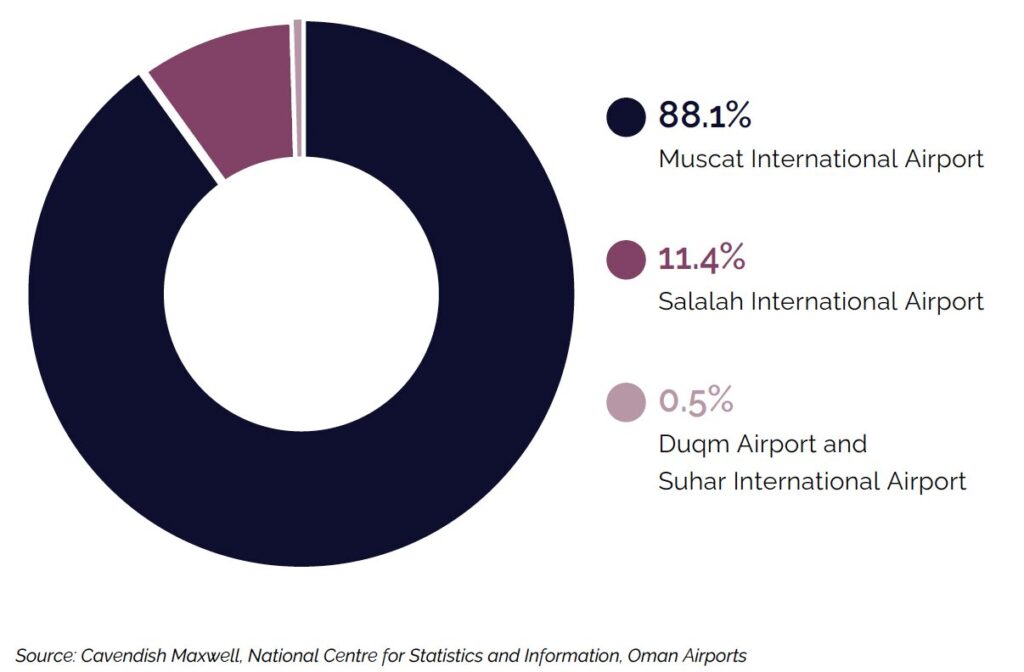

Muscat International Airport solidified its position as the backbone of Oman’s air connectivity, handling 13.2 million passengers and accounting for 88.1% of total traffic, representing a 2.3% increase compared to 2024. Salalah International Airport emerged as the standout performer among secondary hubs, with passenger volumes rising 9.9% year-on-year to 1.7 million (11.4% of total traffic), reflecting Salalah’s strong positioning as a leisure destination. Together, Duqm and Suhar airports accounted for the remaining share of air traffic. However, Suhar International Airport recorded a sharp decline in passenger volumes, primarily driven by a 77.8% reduction in international flight operations.

Airport Passenger Volume by Airports (%)

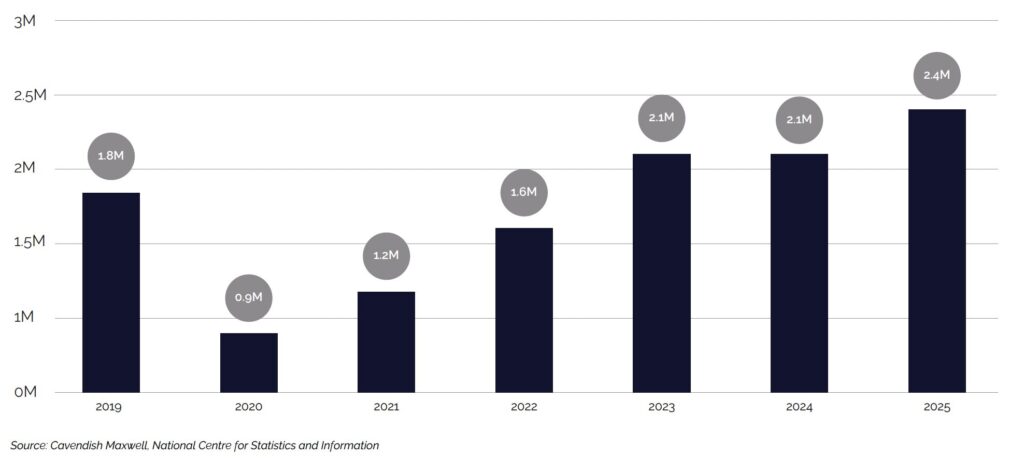

Number of Guests (3-5 Star Hotels)

Oman’s 3–5-star hotel segment maintained its upward trajectory in 2025, welcoming approximately 2.4 million guests over the course of the year, up from 2.1 million in 2024 and representing a 10.8% year-on-year increase. Growth was driven by a rise in both domestic and international arrivals, further bolstered by the Khareef season, which provided a meaningful seasonal uplift to overall guest numbers. Government-led initiatives, including activation programmes and curated events, added further momentum to the sector’s performance. Taken together, these results reinforced Oman’s growing appeal as a destination and reflected a market that steadily broadened its reach, attracting a more diverse guest base throughout the year.

Total Number of Guests in 3-5 Stars Hotel (in Millions)

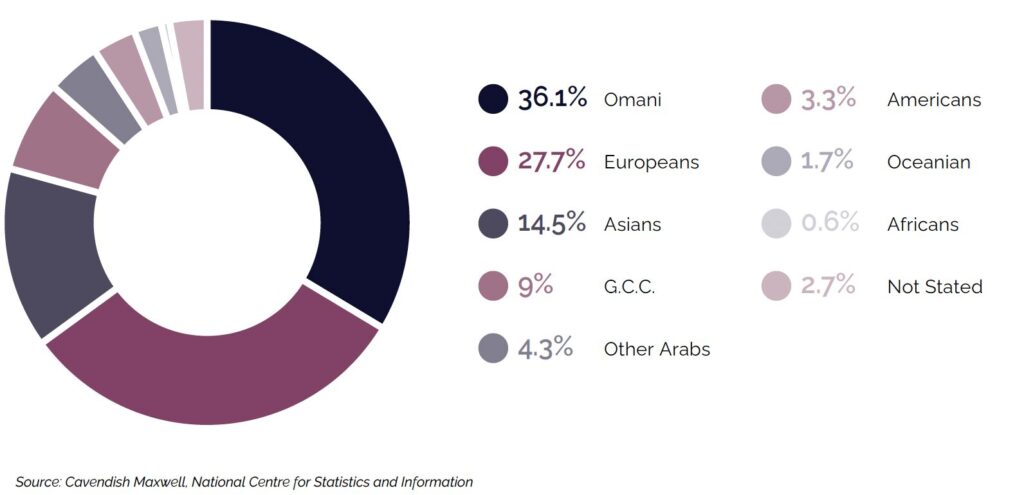

Omani nationals led demand across the 3–5-star segment in 2025, accounting for 36.1% of total guest stays, up from 33.8% in 2024. The 6.6% year-on-year increase reinforced the growing role of domestic tourism in supporting Oman’s hospitality market. Europeans ranked second, contributing 27.7% of total guests and recording a strong 22.3% surge in volumes, while Asian travellers further strengthened their presence, climbing to 14.5% of total guests on the back of an 11% increase. GCC visitors accounted for 9% of total guests, growing 7.2% year-on-year and highlighting the continued importance of regional short-haul travel to Oman’s demand base. Other Arab nationals contributed 4.3%. Rounding out the mix, Americans comprised 3.3% of guests, followed by Oceanians at 1.7% and Africans at 0.6%.

Total Number of Guests in (3-5 Stars) Hotel by Nationality

Oman’s hospitality sector enters this period from a position of strength. We’ve successfully broadened our guest mix, improved occupancy levels, and demonstrated pricing power across our portfolio. Whilst geopolitical developments warrant careful monitoring, our destination’s inherent appeal as a culturally rich, secure haven continues to resonate with travellers. This positions us well to navigate regional uncertainties and sustain growth.

Khalil Al Zadjali

Head of Oman

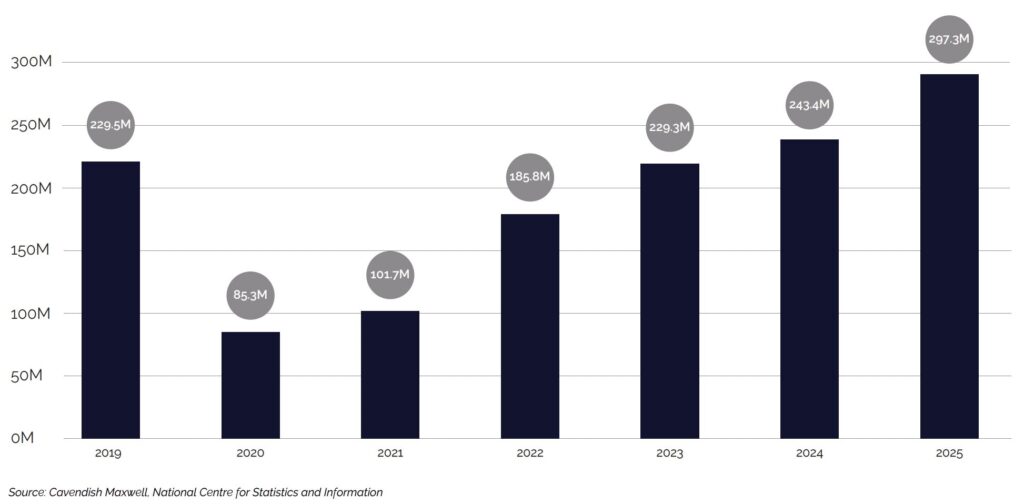

Hotel Revenues (3-5 Star Hotels)

Total hotel revenues in Oman’s 3–5-star segment reached OMR 297.3 million in 2025, up 22.2% year-on-year and marking the highest level in recent years. Room revenues drove this growth, rising 25.8% to OMR 179.1 million, while other revenues contributed OMR 118.2 million, growing 17.1%. The outperformance in room revenues reflected robust demand, supported by higher occupancy rates across the market.

Beyond financial metrics, the sector’s expansion extended to job creation, with employment in 3–5-star hotels rising 7.3% to approximately 11,200 employees. Overall, this performance indicated that growth moved beyond the recovery phase, increasingly driven by structural demand factors, including rising guest volumes, improved occupancy, and a more diversified international visitor base throughout the year.

Total of 3-5 Stars hotel revenue (in Omani Rial Millions)

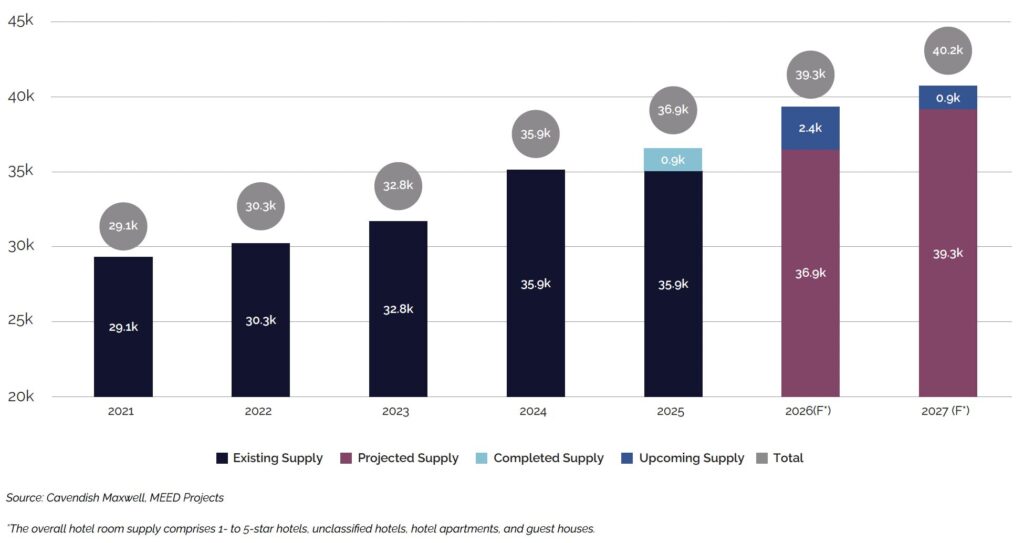

Existing and Future Hotel Room Supply

Oman’s hotel room supply closed 2025 at approximately 36,800 rooms, with around 900 rooms added during the year, falling short of initial projections. While supply growth remained measured in 2025, the pipeline ahead signals a step-up in new capacity, with approximately 2,400 rooms forecasted for delivery in 2026. However, mirroring 2025 trends, actual completions are expected to be lower, followed by a further 900 rooms in 2027.

The expanding pipeline reflects growing developer and investor confidence in Oman’s tourism trajectory, though the phasing of these deliveries will be critical. If new supply is introduced in line with demand growth, the market should be able to absorb additional capacity while maintaining healthy occupancy and revenue performance. At the same time, the influx will broaden accommodation options for visitors, supporting market diversification and competitive balance.

Hotel Room Supply – Number of Rooms (in Thousands) 2025

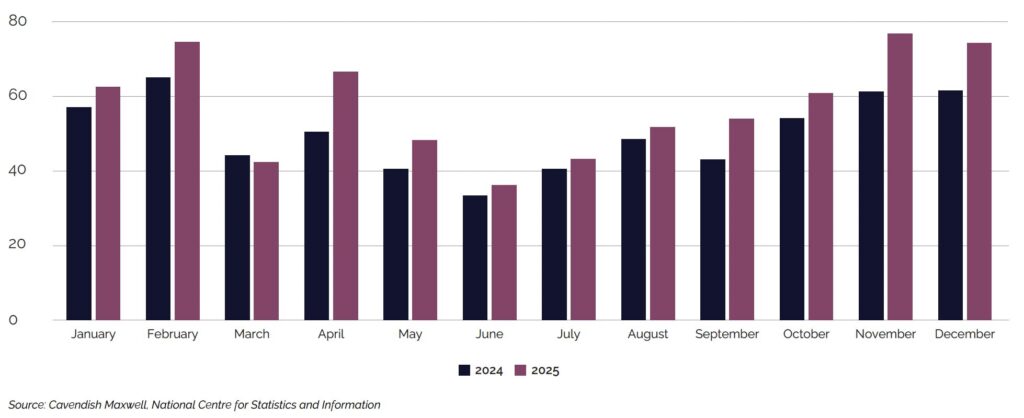

Occupancy Rates (3-5 Star Hotels)

Hotel occupancy across Oman’s 3–5-star segment averaged 56.7% in 2025, up from 49.9% in 2024, marking a 13.6% year-on-year increase. November emerged as the standout performer, recording the highest occupancy of 73.8%, a 17.5% increase over 2024, highlighting Oman’s strengthening appeal as a winter destination. While some seasonal patterns persisted, the market demonstrated notable strength beyond its traditional peak months, with growth registered in shoulder periods as well. The sustained improvement across both peak and shoulder seasons indicated a gradual broadening of the market’s demand profile.

Monthly Occupancy Rates for 3–5 Star Hotels (%)

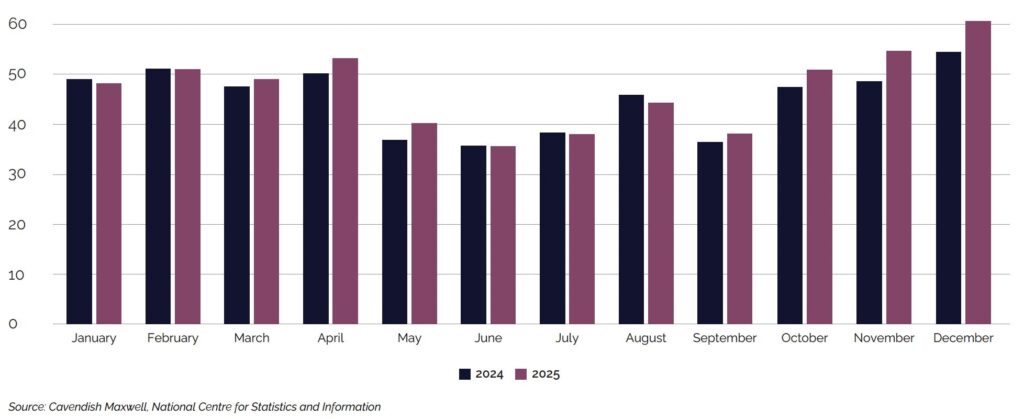

Average Room Rates in Omani Rials (3-5 Star Hotels)

Average room rates (ARR) across Oman’s 3–5-star hotel segment increased by 4.7% in 2025, reaching OMR 48.6. December was the strongest-performing month, with ARR rising to OMR 61.4, up 10.6% year-on-year, followed closely by November at OMR 55.3, which recorded a 13.5% increase. Both winter months continued to command premium rates, highlighting the market’s ability to capitalise on peak-season demand and optimise pricing during periods of elevated occupancy.

Monthly Average Room Rates for 3–5 Star Hotels (in Omani Rials)

Hospitality Market Outlook

Oman’s hospitality sector enters 2026 with strong momentum, having delivered robust performance in 2025, with total hotel revenues reaching OMR 297.3 million, up 22.2% year-on-year. The market has evolved beyond recovery into a phase of sustained growth, supported by a more diversified mix of source markets, rising domestic demand, and improved occupancy levels.

With approximately 2,400 rooms forecast for delivery in 2026 and a further 900 in 2027, the outlook will depend on maintaining demand growth in line with supply expansion. Should guest arrivals continue to grow at rates comparable to the 10.8% increase recorded in 2025, the market is expected to absorb new capacity while maintaining healthy occupancy and revenue performance.

Regional geopolitical developments remain an important consideration, as they may influence international travel patterns and investor sentiment across the region. Tracking shifts in key source markets and financing conditions will therefore be important. Nonetheless, Oman’s differentiated positioning as a culturally rich destination, combined with proactive tourism campaigns and continued infrastructure investment, is expected to support its appeal amid broader regional uncertainty.

Overall, the market remains well-positioned for gradual, sustainable expansion, with the potential to outperform if demand diversification deepens and regional conditions stabilise in the near term.