Dubai Office Market Performance 2025

Executive Summary

Dubai’s office market delivered exceptional performance in 2025, characterised by surging prices, record transaction volumes, and robust rental growth, all supported by strong economic fundamentals and persistent supply constraints. The Emirate’s business ecosystem expanded significantly, with the Dubai Chamber of Commerce registering 71,830 new member companies, pushing total active membership to 292,486, a 13.2% increase year-on-year.

This robust economic backdrop translated directly into market performance. The office sales market recorded its strongest year since 2014, with transaction volumes reaching approximately 4,600 units, a 53.6% increase from 2024. Transaction values surged to AED 13.1 billion, more than doubling from AED 6.5 billion in 2024, representing a 102.3% increase. Sales prices climbed 25.9% to reach AED 1,951 per sq. ft., driven by strong demand from both end-users’ seeking ownership amid rising rents and investors attracted by capital appreciation potential. The rental market mirrored this strength, with citywide rates increasing 22.9% year-on-year as occupancy levels tightened and landlord incentives reduced.

A key factor driving these increases was supply constraint, with only 87,000 sqm delivered from a projected 224,000 sqm pipeline, representing a 39% materialisation rate. Total office stock reached 9.4 million sqm, up just 0.9% from 2024. This supply-demand imbalance kept market conditions firmly tilted in favour of landlords throughout the year.

Looking ahead to 2026, these dynamics are expected to persist. Rental momentum is expected to remain positive, supported by continued business formation and expansion alongside ongoing supply constraints, with only 90,000 to 140,000 sqm expected to materialise from the projected 300,000 sqm pipeline. Whilst the outlook remains positive, several risks warrant monitoring, including potential supply acceleration, global economic headwinds, and geopolitical developments. Nevertheless, Dubai’s strategic positioning as a premier business hub, supported by proactive policies and the Dubai Economic Agenda D33, is expected to provide a robust framework to sustain positive market trajectory throughout 2026.

Dubai Market Snapshot for 2025

- Sales Transaction Volume: ~4,600 (+53.6% Y-on-Y)

- Sales Transaction Value: AED 13.1 Billion (+102.3% Y-on-Y)

- Office Sales Price: +25.9% Y-on-Y

- Office Rental Rate: +22.9% Y-on-Y

- New International Firms: 373

- Multinationals: 64

- SMEs: 309

Dubai’s Economic Growth and Investment Highlights 2025

Dubai’s business ecosystem experienced significant expansion throughout 2025, supported by strong growth in new business registrations and international investment flows. The Dubai Chamber of Commerce registered 71,830 new member companies during the year, pushing total active membership to 292,486, a 13.2% increase from 258,318 members recorded in 2024. Trade activity also reached record levels, with members’ exports and re-exports totalling AED 356.5 billion, representing a 15.1% year-on-year increase and marking the highest value in the chamber’s history.

The Emirate’s appeal to foreign businesses intensified considerably as well, driven by targeted international outreach efforts that positioned Dubai as a premier global business destination and successfully attracted 373 international companies to establish operations in the city. This influx, which included both multinational corporations and Small and Medium Enterprises, represented an 80.2% surge compared to the 207 companies that relocated to Dubai in 2024.

This momentum was further reflected in the performance of other business districts. DIFC recorded a surge in new business registrations, with 2,525 new active companies established, up 38.5% from 2024. Total active registered firms rose to 8,844, reflecting a 27.8% year-on-year increase, while the workforce expanded to 50,200, marking a 9% rise from the previous year. Similarly, Dubai South welcomed 653 new companies during the year, bringing the total number of active businesses to more than 4,200, up 3.9% compared to 2024.

As Dubai continues to enhance its regulatory framework and expand its global connectivity, the city appears well-positioned in the near term to maintain this upward momentum and further consolidate its position as a leading commercial centre in the region.

Sales Transactions

Dubai’s office market recorded a strong uplift in sales activity in 2025, with total transaction volumes reaching approximately 4,600. This marked a 53.6% increase from 2024 and the highest level since 2 014.

The growth was supported by strong demand from end-users turning to ownership amid a tightening rental market, and by investors seeking portfolio diversification under favourable market conditions and strong long-term value potential. While both off-plan and ready segments witnessed growth compared to 2024, the off-plan segment was the main driver of total volume growth, with off-plan activity further intensifying in the second half of 2025.

At the same time, transaction values surged to AED 13.1 billion, up from AED 6.5 billion in 2024. This marked a 102.3% increase, nearly doubling year-on-year.

Sales Transactions – By Volume and Value

![]()

Sales Transactions: Off-Plan vs. Ready

The ready segment continued to dominate the office sales landscape; however, its share declined from 94% in 2024 to 69% in 2025, as off-plan activity surged. The growth in off-plan activity was driven by increased project launches in 2025, with competitive pricing and attractive payment plans that made the segment attractive to buyers. Off-plan transactions jumped from around 177 in 2024 to 1,400 in 2025, a surge of 697.2%. During the same period, ready sales transactions grew by 12.7% to approximately 3,100.

Sales Transactions – By Volume

![]()

“The 2025 performance of Dubai’s office market signals more than a cyclical rebound. It reflects a maturing ecosystem supported by economic diversification, global corporate expansion and constrained Grade A availability. As demand broadens across submarkets, we expect rental resilience and capital appreciation to remain firmly supported.”

Vidhi Shah

Director, Head of Commercial Valuation

In terms of transactional value, the office market more than doubled year-on-year, reaching AED 13.1 billion in 2025, a 102.3% increase driven by robust growth across both segments. Ready office sales values climbed 46.2%, with average transaction prices rising from AED 2.1 million to AED 2.7 million. Meanwhile, off-plan transaction values surged nearly six-fold, jumping from AED 0.7 billion in 2024 to AED 4.6 billion in 2025.

Sales Transactions – By Value (AED Billions)

![]()

Sales Transactions: By Unit Size

In 2025, off-plan office transactions were predominantly concentrated in small to mid-sized units, with offices sized 1,000 to 2,000 sq. ft. accounting for the largest share at 46.6%, closely followed by units below 1,000 sq. ft. at 43.8%. The ready segment mirrored this trend, with offices measuring 1,000 to 2,000 sq. ft. similarly dominating activity at 48.4% of transactions, while units below 1,000 sq. ft. also maintained strong demand at 37.2%. However, across both segments, large offices above 5,000 sq. ft. remained limited, accounting for just 1.5% of off-plan transactions and 1.3% of ready transactions.

![]()

![]()

Sales Transactions: Top 5 Areas by Transactional Volume (Ready)

Ready office transactions were heavily concentrated in core commercial hubs, with Business Bay and Jumeirah Lakes Towers (JLT) together accounting for 73.1% of all ready transactions. This concentration highlights that location, prestige and accessibility remain key considerations for buyers in the ready segment. At the same time, well-connected alternative business districts such as Barsha Heights (Tecom), Dubai Silicon Oasis, and Dubai Investments Park also ranked among the top five submarkets, supported by their more competitive pricing.

- Business Bay

1,230 Transactions - Jumeirah Lakes Towers

1,067 Transactions - Barsha Heights (Tecom)

267 Transactions - Dubai Silicon Oasis

147 Transactions - Dubai Investments Park

92 Transactions

Source: Property Monitor, Cavendish Maxwell

Sales Transactions: Top 5 Areas by Transactional Volume (Off-Plan)

Within the off-plan segment, the top five areas (Motor City, Jumeirah Village Circle, Business Bay, Dubai Sports City, and Majan) accounted for 73.8% of all off-plan office transactions. Notably, Business Bay’s presence among the top off-plan markets, alongside its dominance in ready transactions, reflected strong buyer appetite for the area across both segments.

- Motor City

290 Transactions - Jumeirah Village Circle

202 Transactions - Business Bay

195 Transactions - Dubai Sports City

189 Transactions - Majan

166 Transactions

Source: Property Monitor, Cavendish Maxwell

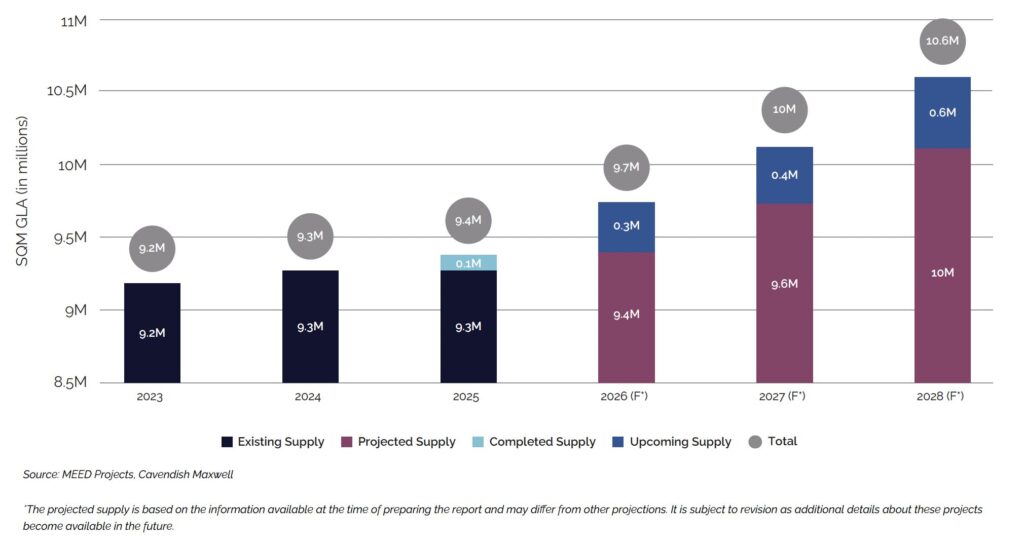

Existing and Future Office Supply

In 2025, Dubai’s total office supply reached 9.4 million sqm, a marginal increase of 0.9% compared to 2024. While approximately 224,000 sqm of new office space was initially projected for delivery during the year, only around 87,000 sqm was completed, bringing the materialisation rate to just 39%.

Looking ahead, around 300,000 sqm of office space is expected to enter the market in 2026. However, based on historical completion patterns, actual deliveries are expected to range between 90,000 sqm to 140,000 sqm, with a portion of the projected supply likely spilling over into 2027 and beyond. Given this constrained supply pipeline and strong occupier demand driven by economic growth and business expansion, the market is expected to remain supply-limited in the near term. This is likely to keep conditions tilted in favour of landlords and support continued upward pressure on rental rates, particularly in prime locations where quality ready stock remains scarce.

Office Supply (in SQM)

Sales Price Trend

Dubai’s office sales prices surged 25.9% in 2025, reaching AED 1,951 per sq. ft., supported by strong interest from both occupiers and investors. Rising rents and reduced landlord incentives prompted some occupiers to buy rather than lease. At the same time, investors also participated in the market aggressively, attracted by the strong rental environment and ongoing capital appreciation. This heightened demand, combined with limited inventory in prime locations, intensified competition, and fuelled price appreciation.

Sales Price Trend

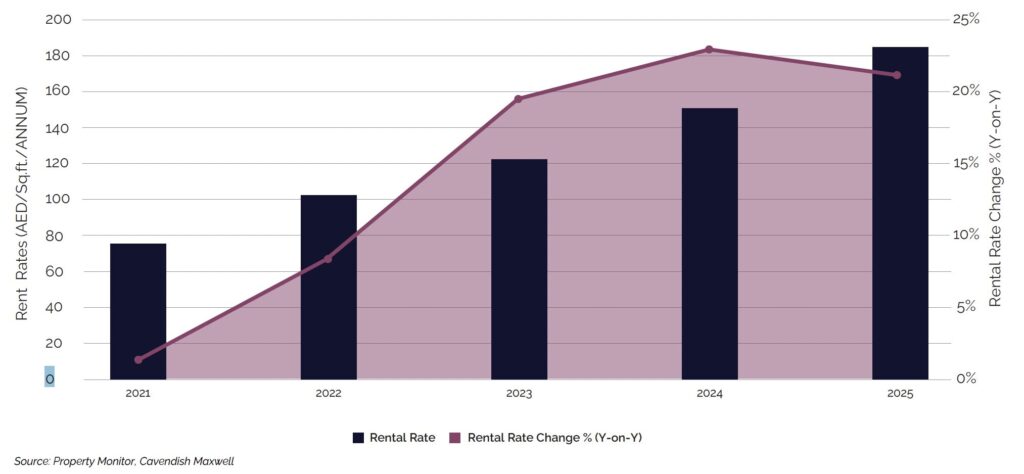

Rental Rate Trend

In parallel with the rise in office sales prices, Dubai’s office rental market saw robust growth in 2025, driven by increasingly tight occupier conditions as occupancy levels continued to rise across the city. This dynamic further strengthened the already landlord-favoured market, resulting in a reduction in leasing incentives. At the citywide level, office rental rates increased by 22.9% year-on-year.

Rental Rate Trend

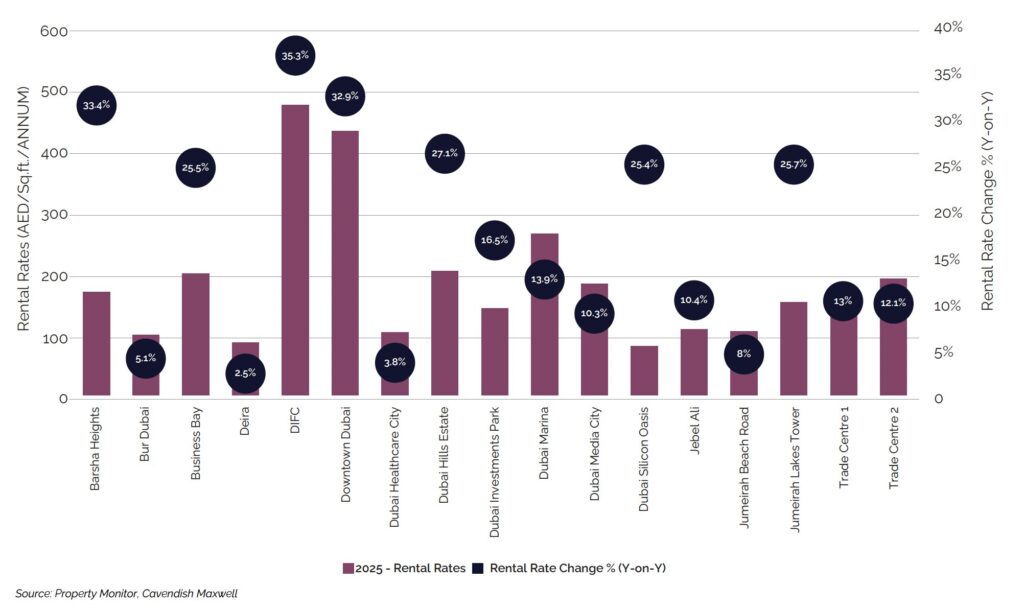

Rental Rate Change by Area (2024 vs. 2025)

While rental growth was observed across the city, the pace varied significantly by location. DIFC and Downtown Dubai, the city’s core business districts, recorded above-average year-on-year increases of 35.3% and 32.9%, respectively. This performance was driven by tightening occupancy levels, limited availability of Grade A office stock and strong demand for prestigious, centrally located space. Constrained conditions in these core CBD locations generated spillover demand into well-connected sub-markets, with Barsha Heights emerging as a key beneficiary, recording rental growth of 33.4%. Similarly, Dubai Hills Estate, Business Bay, Jumeirah Lakes Towers, and Dubai Silicon Oasis posted robust rental increases ranging between 25% and 27%, as tenants sought high-quality alternatives without the premium pricing associated with core CBD locations. In contrast, more mature sub-markets with older office stock, such as Bur Dubai and Deira, experienced more modest rental growth of 5.1% and 2.5%, respectively, as demand in these areas remained largely driven by cost-sensitive occupiers and locally oriented businesses.

Rental Rate Movement in 2025

2026 Real Estate Market Outlook

The market dynamics anticipated for 2025 largely materialised, with both sales prices and rental rates surging across the city. Sales performance was particularly strong, with transaction volumes reaching their highest level in over a decade. This was driven by robust demand from investors and end-users alike, the latter increasingly opting for ownership as an alternative to rising rental costs in a tightening rental market.

Entering 2026, these conditions are expected to persist. Off-plan activity, which accelerated in 2025, is expected to remain elevated throughout the year as developers respond to improved demand visibility and heightened pricing confidence. With high-quality ready stock still severely constrained, off-plan launches are expected to continue absorbing demand from buyers seeking viable entry points into the market.

Rental momentum is also expected to remain positive, supported by high occupancy levels and ongoing supply constraints, as only 90,000–140,000 sqm is expected to materialise from the projected 300,000 sqm pipeline. Grade A offices are expected to continue outperforming the broader market, driven by occupier preference for quality, efficiency, and sustainability. Meanwhile, the spillover effect observed in 2025 is expected to persist, with Grade B assets in well-connected submarkets continuing to appeal to cost-conscious tenants, particularly in locations offering better value propositions.

Whilst the outlook remains positive, several factors warrant monitoring. Accelerated supply completions could moderate growth trajectories, though current delivery patterns suggest this remains unlikely. Global economic headwinds, shifts in international investment flows, or geopolitical developments may also affect Dubai’s attractiveness as a business destination and dampen occupier demand. Nevertheless, Dubai’s strategic positioning as a premier global business hub, supported by proactive Government policies, world-class infrastructure, and the ambitious Dubai Economic Agenda D33, provides a strong foundation to navigate these challenges and sustain the market’s positive trajectory.