Dubai Office Market Performance Q1 2026

Executive Summary

Dubai’s office market recorded a strong start to 2026, supported by continued business formation and sustained investor interest. Despite regional tensions escalating in March, business inflows remained resilient, with the Dubai Chamber of Commerce registering 2,709 new member companies during the month alone. This momentum was reflected in DIFC, which attracted 775 new companies across the quarter, with March emerging as its strongest month at 258 new registrations, up 59% year-on-year, further reinforcing Dubai’s standing as the region’s preferred business destination.

Transaction activity reflected this broader strength, with approximately 1,600 transactions recorded in Q1 2026 and total transaction values reaching AED 8.2 billion. Activity was, however, unevenly distributed across the quarter, with the bulk of momentum concentrated in January and February before easing in March. Within this, the off-plan segment outperformed, accounting for 60.7% of total volumes, driven by new project launches and continued investor appetite, while ready transactions softened over the same period.

On the supply side, conditions remained relatively controlled. Approximately 73,300 sq. m. was delivered in Q1 2026, including the completion of DIFC Square, a Grade A development that was fully pre-leased prior to handover. A further 240,000 sq. m. is expected to be delivered through the remainder of 2026, bringing total stock to approximately 9.7 million sq. m. by year-end, with the pipeline expanding further through 2027 and 2028.

Against this backdrop, pricing performance remained strong. Office sales prices rose 22.9% year-on-year to AED 2,029 per sq. ft., while rental rates increased 20% year-on-year to AED 191.9 per sq. ft., supported by tight vacancy in Grade A stock and a continued occupier preference for well-located, high-quality space. Growth was most pronounced in established business districts, with DIFC and Downtown Dubai leading rental appreciation across the market.

Looking ahead, Dubai’s office market is expected to remain supported by structural demand drivers, although activity levels may become more measured as occupiers and investors adjust to a more complex external environment. Rental growth is expected to normalise as additional supply enters the market from late 2026 onwards, while Grade A assets are likely to continue outperforming secondary stock. Overall, the medium-term outlook remains broadly positive, supported by Dubai’s positioning as a regional business hub and ongoing policy support.

Market Snapshot for Q1 2026

Dubai’s Economic and Investment Highlights Q1 2026

Despite regional tensions escalating in March, Dubai’s business environment demonstrated notable resilience. The Dubai Chamber of Commerce registered 2,709 new member companies during the month, while DIFC attracted 775 new companies in Q1 2026, a 62% increase on the same period in 2025. Notably, March was DIFC’s strongest month of the quarter with 258 new companies, up 59% year-on-year, suggesting that even as broader market activity slowed, businesses continued to actively choose Dubai as their base of operations.

The broader macroeconomic context, however, warrants attention. The UAE’s GDP growth outlook has been revised downward from 5.6% to 3.1% for 2026, reflecting the economic impact of ongoing regional tensions. Growth across the Middle East is now projected at approximately 1.8% for 2026, down from 4.0% in 2025 according to the World Bank, driven by the closure of the Strait of Hormuz, disruptions to energy infrastructure, and heightened financial volatility across the region.

Business activity indicators echoed this more cautious tone. Dubai’s PMI eased from 54.6 in February to 53.2 in March, with new orders slowing to a seven-month low. The impact of regional tensions was most visible in supplier delivery times, which lengthened at the fastest pace since mid-2022, and in business confidence, which fell to its lowest level since April 2023. In response, Dubai announced a new AED 1 billion fiscal support package aimed at reinforcing business confidence and sustaining economic resilience.

Despite these headwinds, Dubai’s underlying economic fundamentals remain stable, supported by continued business formation, infrastructure investment, and government support measures.

Looking ahead, Dubai’s office market is expected to remain resilient, as demand fundamentals remain in place thanks to the city’s regulatory environment, tax competitiveness and quality of infrastructure. While the pace of sales and leasing activity could become more measured in the near term, government policy is expected to provide meaningful support to the market.

Vidhi Shah

Director, Head of Commercial Valuation

Sales Transactions

Dubai’s office market recorded a strong start to 2026, with approximately 1,600 transactions in Q1 2026, reflecting a 74.6% year-on-year increase and a 1.8% quarter-on-quarter rise. Transaction values reached AED 8.2 billion, up 203.5% annually and 72.8% compared to Q4 2025, highlighting sustained demand across the sector driven by ongoing business formation and international corporate expansion.

However, activity was heavily concentrated in the early part of the quarter, with January and February accounting for 83% of total transaction volumes and 81.1% of total value. This strong momentum eased in March 2026, when transaction volumes declined by 13.4% year-on-year, largely driven by a 63% drop in ready transactions. In contrast, off-plan transactions rose by 127.5%, although this should be interpreted with caution given the longer registration lag in this segment, meaning March figures reflect transactions agreed both prior to and during the early stages of the geopolitical tensions.

While the March slowdown may appear linked to external developments, seasonal factors such as the timing of Ramadan also contributed. The coming months are expected to provide a clearer view of und erlying demand once seasonal and timing effects normalise.

Sales Transactions – By Volume and Value

![]()

Sales Transactions: Off-Plan vs. Ready

The off-plan segment continued to drive activity in Q1 2026, recording around 950 transactions, up 490.7% year-on-year and 27.3% quarter-on-quarter. Notably, this marked the first time since Q3 2010 that off-plan sales overtook ready transactions in a single quarter, accounting for 60.7% of total volumes. Much of this momentum was concentrated in a single project, with Shahrukh by Danube alone accounting for around 40% of all off-plan transactions during the quarter. Ready transactions, meanwhile, declined 16.4% year-on-year and 22.3% quarter-on-quarter to 615 units, a softening largely driven by the slowdown in activity seen in March.

Sales Transactions – By Volume

![]()

On the value side, off-plan transactions reached AED 6.4 billion in Q1 2026, representing a 760.6% increase year-on-year and a 165.4% rise quarter-on-quarter. Ready transaction values, by contrast, declined 8.5% year-on-year and 23.1% quarter-on-quarter to AED 1.8 billion, consistent with the broader softening in ready activity seen during the quarter. At the monthly level, total transaction values in March 2026 rose 59.7% year-on-year, driven by the off-plan segment, where values surged 191%, while ready transaction values declined 54.8% over the same period.

Sales Transactions – By Value (AED Billions)

![]()

Sales Transactions by Unit Size

Within the off-plan segment, small to mid-sized units dominated activity, with units below 2,001 sq. ft. accounting for 74.4% of off-plan transactions. However, larger units above 5,000 sq. ft. gained notable prominence in Q1 2026, rising to 7.3% of off-plan transactions, up from just 1.5% in 2025, reflecting a growing appetite for more spacious office product. The ready segment followed a similar pattern, with units below 2,001 sq. ft. accounting for 88.3% of ready transactions.

Off-Plan Sales Transactions by Unit Size (%)![]()

Ready Sales Transactions by Unit Size (%)

![]()

Top 5 Areas with the Highest Transactions

Combined Ready and Off-Plan Transactions

In Q1 2026, sales activity remained highly concentrated, with the top five locations accounting for 71.5% of all transactions. Al Sufouh 1 led the rankings, driven by strong off-plan demand in the area, while Business Bay performed strongly across both the off-plan and ready segments. Jumeirah Lakes Towers continued to reflect sustained buyer appetite for established, well-connected commercial hubs.

- Al Sufouh 1

390 Transactions - Business Bay

373 Transactions - Jumeirah Lakes Towers

223 Transactions - Dubai Maritime City

78 Transactions - Trade Center 2

71 Transactions

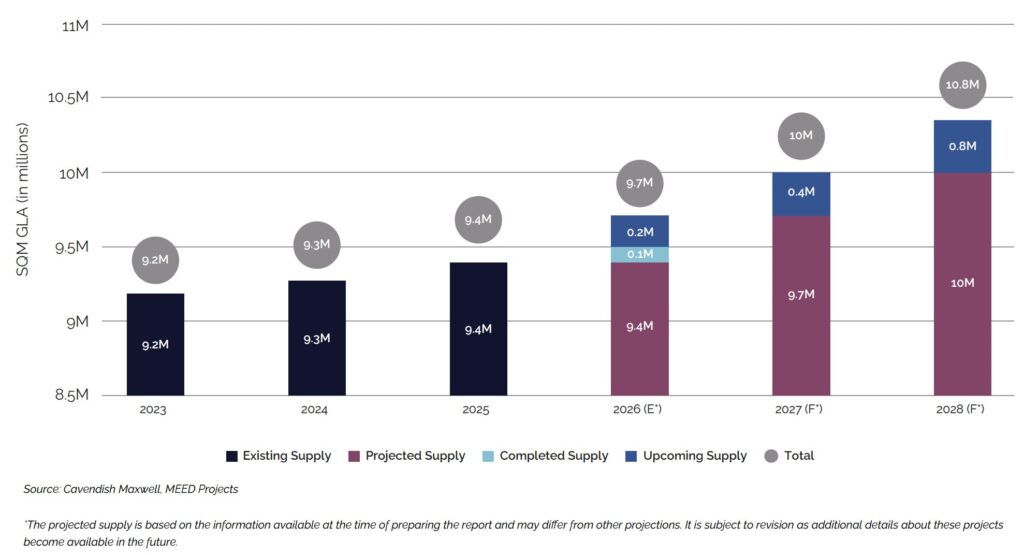

Existing and Future Office Supply

Dubai’s office supply has expanded steadily in recent years, increasing from 9.2 million sq. m. in 2023 to 9.4 million sq. m. in 2025. This relatively measured pace of new supply has helped support growth in both sales prices and rental rates across the market.

In Q1 2026, supply expanded further, with approximately 73,300 sq. m. completed. This included the delivery of DIFC Square, a 55,700 sq. m. Grade A office development that was completed ahead of schedule and fully pre-leased prior to handover. A further 240,000 sq. m. of supply is expected to be delivered during the remainder of 2026, which would bring total office stock close to 9.7 million sq. m. by year-end. However, only 23.6% of expected 2026 supply has been delivered so far.

Looking ahead, the pipeline is expected to expand more noticeably from 2027 onwards, with total office stock projected to reach approximately 10.0 million sq. m. by 2027 and 10.8 million sq. m. by 2028. While ongoing regional tensions could potentially affect construction timelines through supply chain disruptions, rising material costs, and logistical challenges, much of the upcoming pipeline consists of committed projects already under construction, with financing and contractors already in place. As a result, any impact is more likely to lead to delivery delays rather than widespread project cancellations, although the situation warrants close monitoring as the year progresses.

Office Supply (in SQM)

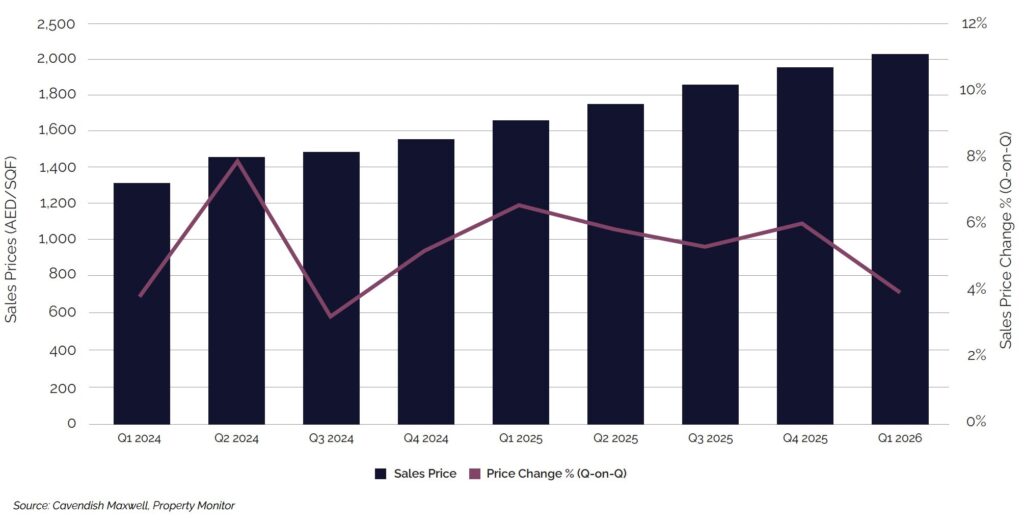

Sales Price Trend

Sales prices in Dubai’s office market continued to appreciate in Q1 2026, recording a 22.9% year-on-year increase, with prices reaching AED 2,029 per sq. ft., even as transaction activity slowed in March. Looking ahead, the trajectory of prices will largely depend on how regional developments unfold and the degree to which buyer confidence holds, with the coming quarters expected to provide a clearer indication of market direction.

Sales Price Trend

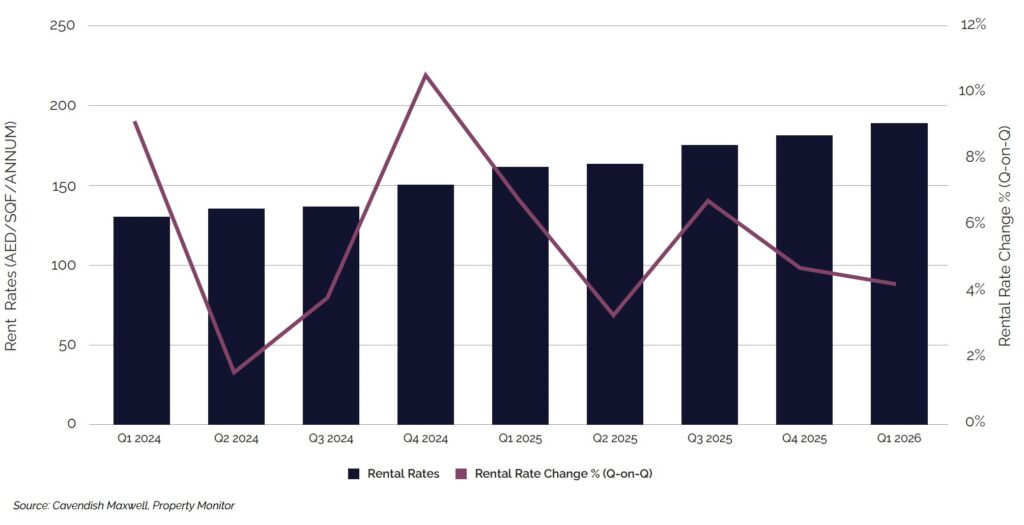

Rental Rate Trend

Office rental rates remained firm in Q1 2026, rising 20% year-on-year to reach AED 191.9 per sq. ft., even as leasing activity showed some moderation during the quarter. Landlords continued to maintain asking rents, supported by the scarcity of quality office space, particularly Grade A stock in well-connected, established business districts where vacancy remains tight.

Rental Rate Trend

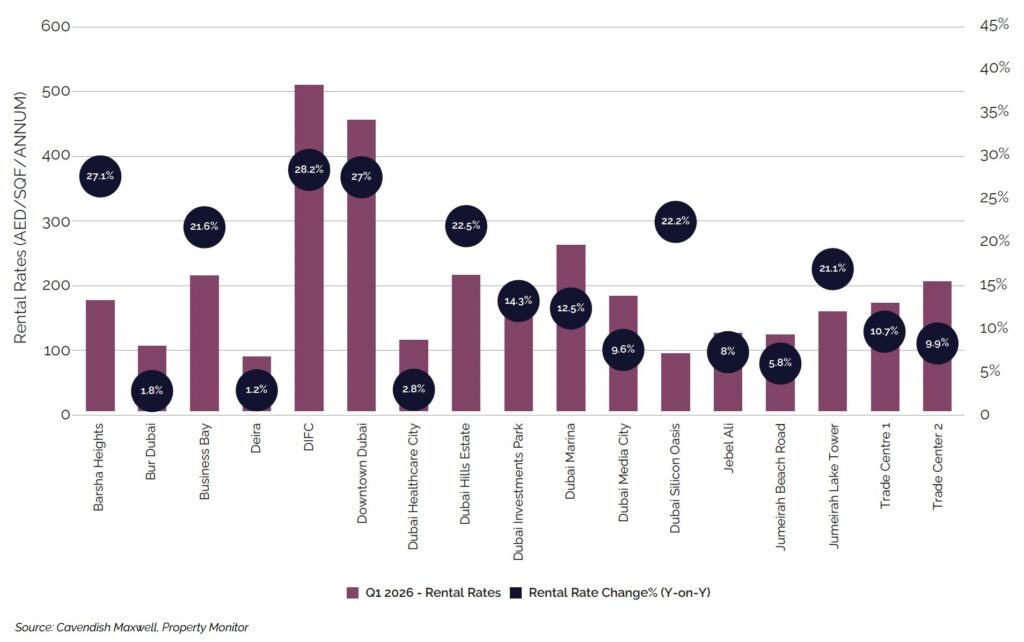

Rental Rate Change by Area (Q1 2025 vs. Q1 2026)

Office rental rates recorded broad-based growth across most submarkets in Q1 2026, with established office locations leading the way. DIFC (+28.2%) and Downtown Dubai (+27.0%), the city’s core business districts, recorded some of the strongest increases, reflecting continued demand for high-quality, centrally located office space. Business Bay (+21.6%) also posted strong growth, benefiting from spillover demand. Other established areas, including Barsha Heights (+27.1%), Dubai Silicon Oasis (+22.2%), and Jumeirah Lakes Towers (+21.1%), also recorded notable growth as occupiers sought high-quality alternatives. In contrast, older and more peripheral office stock such as Dubai Healthcare City (+2.8%), Bur Dubai (+1.8%), and Deira (+1.2%) saw more moderate movement.

Rental Rate Movement in Q1 2026 Q1

2026 Real Estate Market Outlook

As 2026 progresses, Dubai’s office market is expected to remain broadly resilient, although it is now operating within a more complex external environment than anticipated at the start of the year. Underlying demand fundamentals remain evident, supported by the Emirate’s regulatory environment, tax competitiveness, and infrastructure quality. However, the pace of transaction and leasing activity may become more measured in the near term, as investors and occupiers adopt a more selective approach and decision-making timelines extend while the broader regional picture continues to evolve.

The flight to quality is expected to become more pronounced as the year progresses. The divergence in rental growth already visible across submarkets is likely to widen further, with Grade A office space in established business districts continuing to attract the strongest occupier demand. In contrast, older and secondary stock may face increasing competitive pressure, particularly as occupiers place greater emphasis on building quality, amenities, and connectivity.

Rental growth is expected to remain positive, although at a more measured pace compared to recent years. The strong rental increases recorded across core office submarkets in 2024 and 2025 reflected a market responding to years of limited supply alongside a significant increase in occupier demand. With additional supply expected to enter the market from late 2026 and more substantially through 2027 and 2028, rental growth is likely to normalise rather than continue at the elevated pace seen over the past two years. Nevertheless, landlords within well-positioned and highly occupied offices are expected to retain pricing power.

Government policy is also expected to provide meaningful support to the market. The AED 1 billion fiscal support package announced earlier in 2026, combined with Dubai’s established track record of proactive policy intervention, provides an important buffer against downside risks. The government’s ability to support economic activity, streamline business licensing, and attract investment through regulatory reform remains one of Dubai’s key competitive advantages.

Despite the more challenging external backdrop, the medium-term outlook for Dubai’s office market remains broadly positive. While conditions may become more measured in the near term, the underlying drivers supporting office demand remain in place.