Abu Dhabi Residential Market Performance Q1 2026

Executive Summary

Abu Dhabi’s residential market delivered a record-breaking start to 2026, despite a more challenging macroeconomic backdrop. Approximately 8,100 residential sales transactions were recorded in Q1 2026, representing a 123.6% increase compared to the same period last year, with total sales value reaching AED 38.1 billion, the highest quarterly figure on record and a 211.5% increase year-on-year. Market activity continued to be dominated by the off-plan segment, which accounted for over four-fifths of all residential transactions and nearly 90% of total sales value, supported by new project launches and strong interest from both domestic and international buyers.

Apartments remained the primary driver of market activity, accounting for 70.7% of all residential sales transactions, with demand particularly concentrated across Al Reem Island, Yas Island and Saadiyat Island. Hudayriyat Island emerged as the most active villa and townhouse market, supported by strong activity within Modon developments. The strength of transactional activity translated into broad-based price growth, with apartment sales prices increasing by 17.1% year-on-year and villa prices rising by 10.9%. Rental market performance also remained positive, with apartment and villa rents increasing by 10.5% and 4.4%, respectively, indicating that occupier demand has remained firm despite ongoing additions to residential stock.

Looking ahead, while Q1 2026 performance suggests that market fundamentals remain robust, the coming quarters will be critical in assessing whether this momentum reflects durable underlying demand. As both off-plan and ready transactions typically exhibit reporting lags, additional data will be required to fully assess the impact of recent geopolitical developments on underlying demand conditions.

Market Snapshot for Q1 2026

Macroeconomic Overview and Outlook

Abu Dhabi entered 2026 building on a strong 2025, with S&P estimating GDP growth of 5.3% for the prior year, supported by robust non-oil sector expansion, rising government expenditure, and continued progress on the emirate’s economic diversification agenda. However, the growth outlook was revised downward in March 2026, with initial projections of 5.8% to 6.2% adjusted to 2.2% following the escalation in regional geopolitical tensions and growing uncertainty around maritime trade routes through the Strait of Hormuz. While elevated oil prices are expected to provide a near-term fiscal tailwind, supporting government spending capacity and investor confidence, the same geopolitical backdrop introduced headwinds around business sentiment and forward planning that tempered the broader growth outlook.

Looking ahead, the pace of expansion will largely depend on how regional conditions evolve and whether stability across energy markets and global trade routes can be maintained. Abu Dhabi’s ongoing diversification efforts and long-term infrastructure investment are expected to provide a buffer against oil price volatility, positioning the emirate to sustain medium-term growth in a more constrained global environment. The foundations built through 2025 leave Abu Dhabi better placed than most to navigate the current period of uncertainty.

The Abu Dhabi property market maintained strong momentum in Q1 2026, with continued demand driving growth across both sales and rental segments. The consistent sell-out of off-plan projects highlights the solid fundamentals underpinning the market. While transaction levels may not match the exceptional performance seen in Q4 2025, it is important to recognise that 2025 represented an outstanding year for Abu Dhabi real estate. Overall, the key themes for Q1 2026 are modest growth, resilience, and stability.

Andrew Laver

Director, Commercial Valuation – Abu Dhabi

Sales Transactions

Sales Transactions: By Volume

Abu Dhabi City’s residential market opened 2026 with its strongest first quarter on record, registering approximately 8,100 sales transactions, an increase of 123.6% compared to Q1 2025. The quarter was once again dominated by the off-plan segment, which accounted for 81.6% of all residential sales activity. Off-plan transactions reached approximately 6,600 in Q1 2026, rising by 184.4% year-on-year, supported by new project launches and strong demand from both domestic and international buyers. The ready segment also recorded growth, with transactions increasing by 14.8% year-on-year to approximately 1,500 sales. While overall transaction volumes were 3.8% lower than the levels achieved in Q4 2025, the decline was consistent with the seasonal patterns observed in previous years, where activity typically moderates in the first quarter following a strong year-end performance. As such, the quarterly decline was more reflective of normal market seasonality than any weakening in underlying demand.

At a monthly level, March 2026 recorded approximately 2,500 residential sales transactions, comprising around 2,100 off-plan and 400 ready home sales. Transaction activity increased by 126.9% compared to March 2025, largely driven by a 208.1% year-on-year increase in off-plan sales. The strong performance was particularly noteworthy given that the month coincided with the Ramadan and Eid period, which has historically resulted in slower market activity. Despite seasonal factors and heightened regional geopolitical uncertainty during the month, residential transaction volumes remained resilient. However, the strength of the off-plan segment should be interpreted with some caution, as off-plan transactions typically involve a longer registration lag. As a result, the March transaction figures likely capture purchasing decisions made both before and during the initial period of heightened geopolitical uncertainty. The coming months are expected to provide a clearer indication of underlying demand once seasonal influences and registration timing effects have normalised.

Abu Dhabi City Unit Sales Transactions – By Volume

![]()

Sales Transactions: By Value

The strength observed in transaction volumes during Q1 2026 was mirrored in transaction values, with Abu Dhabi City’s residential market recording a total sales value of AED 38.1 billion during the quarter. This represented an increase of 211.5% compared to Q1 2025 and 34.9% compared to Q4 2025, marking the highest quarterly residential sales value on record. The strong performance was driven largely by activity in February 2026, which recorded the highest monthly residential sales value ever registered in the emirate. The off-plan segment continued to dominate market activity, accounting for 89.3% of the total residential sales value in Q1 2026. Off-plan sales value reached AED 34 billion, increasing by 279.2% year-on-year and 44.2% quarter-on-quarter. Meanwhile, the ready segment recorded AED 4.1 billion in sales value, representing a 25.2% increase compared to Q1 2025, although values were 12.2% lower than the previous quarter.

At a monthly level, residential sales value totalled AED 11.4 billion in March 2026, an increase of 222.7% compared to March 2025. Similar to the broader quarterly trend, growth was primarily driven by the off-plan segment, where transaction values rose by 327.7% year-on-year to AED 10.4 billion. In contrast, the ready segment recorded AED 1.1 billion in sales value, representing a marginal decline of 4.8% compared to March 2025.

Abu Dhabi City Unit Sales Transactions – By Value (AED)

![]()

Sales Transactions by Property Type: Apartments

Apartments continued to capture an increasing share of residential sales activity in Abu Dhabi City, accounting for 70.7% of all transactions in Q1 2026, up from 68.8% a year earlier. This translated into approximately 5,700 apartment sales during the quarter, representing a 130% increase compared to Q1 2025 and a 25.3% rise from Q4 2025. Growth was driven primarily by the off-plan segment, where transaction volumes surged by 181.3% year-on-year to approximately 4,600 sales. The concentration of recent apartment launches played a key role in supporting activity, while the segment’s relatively lower entry price points continued to make it accessible to a broader range of buyers. Meanwhile, the ready apartment segment recorded approximately 1,100 transactions, declining by 15.5% quarter-on-quarter from Q4 2025 but remaining 30.2% higher than Q1 2025 levels.

Abu Dhabi City Apartment Transactions – By Volume

![]()

Sales Transactions by Property Type: Villas and Townhouses

Villa and townhouse sales remained strong in Q1 2026, with approximately 2,400 transactions recorded during the quarter, representing a 109.6% increase compared to Q1 2025. While transaction volumes declined by 38.4% compared to Q4 2025, activity remained well above historical levels and significantly higher than the same period last year. The off-plan segment continued to account for the majority of transactions, with volumes increasing by 191.9% year-on-year to approximately 2,000 sales. The ready segment recorded approximately 400 transactions, declining by 14.0% year-on-year and 12.2% quarter-on-quarter.

Abu Dhabi City Villa/Townhouse Transactions – By Volume

![]()

Sales Transactions by District

Al Reem Island remained the most active apartment market in Abu Dhabi City, recording approximately 1,990 transactions in Q1 2026, an increase of 224.2% compared to the same period last year. Yas Island followed with around 1,500 transactions, while Saadiyat Island, Khalifa City and Fahid Island completed the top five most active apartment locations. Collectively, these five areas accounted for 80.6% of all apartment sales transactions during the quarter. In the villa and townhouse segment, Hudayriyat Island emerged as the most active location in Q1 2026, supported by strong sales activity across Modon developments. The area accounted for 45.1% of all villa and townhouse transactions during the quarter.

Sales Transactions by Volume: Top 5 Districts – Apartments

![]()

Sales Transactions by Volume: Top 5 Districts – Villas and Townhouses

![]()

Existing and Future Residential Supply

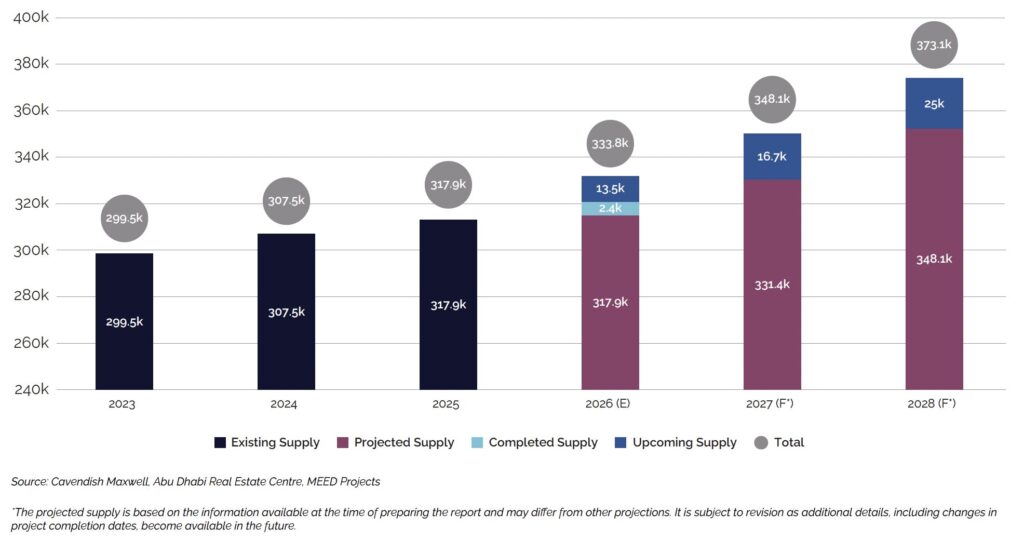

Abu Dhabi City’s residential stock continued to expand in Q1 2026, reaching approximately 320,300 units. Around 2,400 residential units were delivered during the quarter, representing a materialisation rate of 42.3%, with a further 13,500 units currently scheduled for completion over the remainder of 2026. Looking ahead, the development pipeline remains active, with an additional 16,700 units expected in 2027 and nearly 25,000 units projected for delivery in 2028.

As a result, Abu Dhabi City’s total residential inventory is forecast to increase to approximately 373,100 units by 2028, representing an addition of more than 55,000 units compared to current stock levels. Despite the scale of upcoming supply, market fundamentals remain supportive, with recent sales and rental market performance indicating that demand has thus far kept pace with new deliveries. Nevertheless, the timing of future completions will remain an important factor to monitor. While delivery schedules may shift as projects advance through construction, such delays are more likely to defer supply rather than remove it altogether, particularly given that a significant share of the pipeline is already under construction.

Abu Dhabi Supply – Number of Units

Sales Price Change

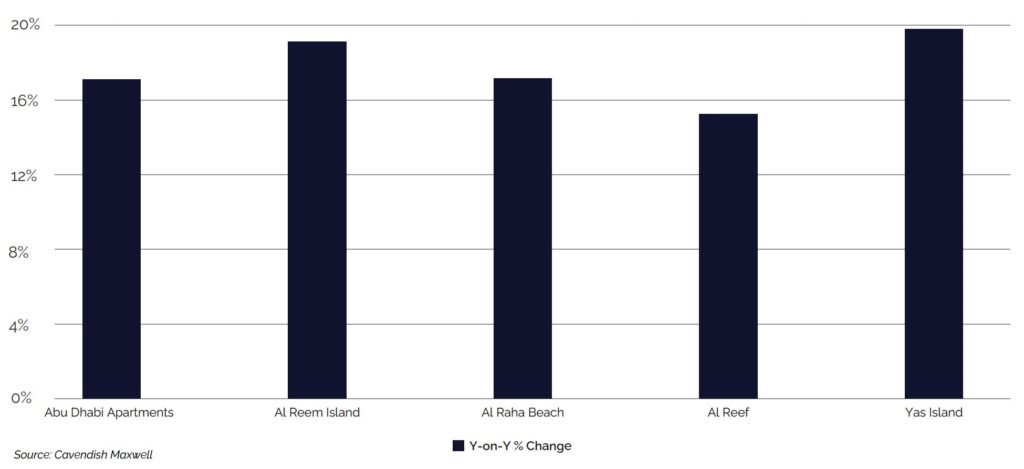

Apartment sales prices across Abu Dhabi City continued to trend upward in Q1 2026, supported by strong buyer demand and record transaction activity. Average apartment prices rose by 17.1% year-on-year, with all tracked submarkets recording positive annual growth. Among the key locations, Yas Island led price appreciation, with values increasing by 19.9% year-on-year, closely followed by Al Reem Island at 19.1%, while Al Raha Beach and Al Reef recorded gains of 17.7% and 15.4%, respectively. This broad-based growth reflects the segment’s appeal to both investors, attracted by relatively accessible entry price points and strong rental income potential, and end-users, particularly smaller families and single-person households, for whom apartments remain a preferred housing option.

Apartment Sales Price Change (%)

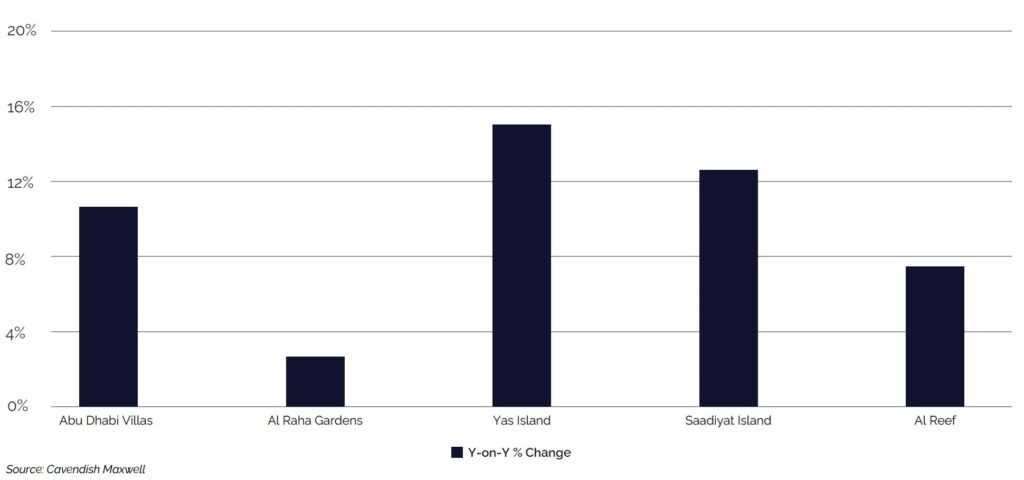

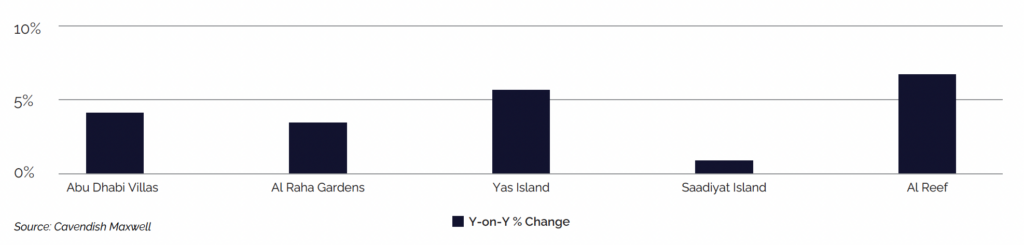

Villa sales prices across Abu Dhabi City continued to strengthen in Q1 2026, with average values increasing by 10.9% year-on-year, although price growth was more moderate than that recorded in the apartment segment. Yas Island recorded the strongest growth, with villa prices increasing by 15.1% year-on-year, followed by Saadiyat Island at 12.2%. Al Reef and Al Raha Gardens also posted gains of 7.5% and 3.1%, respectively. The continued increase in villa values reflects steady demand from end-users, particularly larger families seeking additional living space and community-oriented residential environments.

Villa Sales Price Change (%)

Rental Rates Change

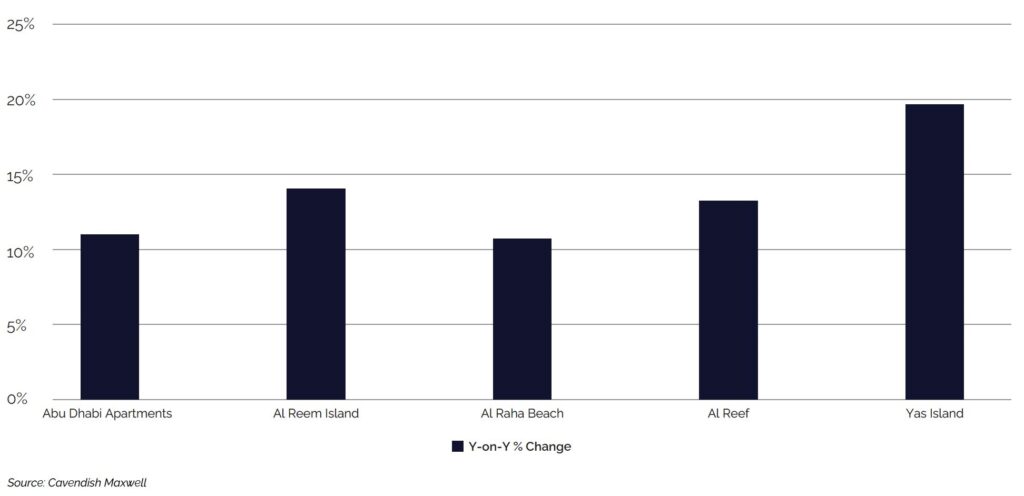

Apartment rental rates across Abu Dhabi City increased by 10.5% year-on-year in Q1 2026, with the strongest growth recorded in Yas Island, Al Reem Island and Al Reef. Abu Dhabi’s growing resident population continued to support demand for residential units, contributing to rental growth across the apartment segment even as new supply continued to enter the market.

Apartment Rental Rate Change (%)

Villa rental rates across Abu Dhabi City rose by 4.4% year-on-year in Q1 2026. Compared to the apartment segment, rental growth within the villa market remained more measured, reflecting the higher cost of occupancy and the relatively smaller pool of tenants seeking larger family homes. Despite this, rental values increased across the emirate, indicating that demand for family-oriented housing has remained steady.

Villa Rental Rate Change (%)

2026 Real Estate Market Outlook

Abu Dhabi’s residential market entered 2026 with strong momentum, even as the macroeconomic backdrop became more cautious following a downward revision in GDP growth expectations to 2.2%, from earlier forecasts of 5.8%–6.2%. The revision reflects heightened geopolitical uncertainty and increased volatility around regional trade routes, which have introduced greater caution into the broader economic outlook. Against this backdrop, the real estate market has continued to demonstrate strong performance.

Q1 2026 marked the strongest first-quarter performance on record, with both transaction volumes and values reaching new highs, supported primarily by strong off-plan activity across key residential communities. This makes the coming quarters important in assessing underlying demand conditions, as both off-plan and ready transactions typically exhibit reporting lags. As a result, Q1 2026 transaction data likely included deals that were agreed prior to, as well as during, the initial period of heightened geopolitical uncertainty, making it more difficult to isolate the immediate impact of changing macro conditions.

Looking ahead, market conditions will be shaped by the interaction between macroeconomic uncertainty, the timing of supply delivery, and underlying demand trends. While geopolitical risks and trade-related uncertainty may temper sentiment at the margin and lead to more selective decision-making, activity in the off-plan segment will continue to be influenced by the pace and scale of new project launches, given its strong reliance on launch-driven momentum.

Overall, while the full impact of current conditions remains to be seen, the exceptionally strong growth phase seen in early 2026 is expected to gradually normalise as the effects of earlier launches, macro uncertainty, and ongoing supply delivery converge.