Ras Al Khaimah Residential Market Performance 2025

Executive Summary

Ras Al Khaimah’s macroeconomic environment remained strong in 2025, with Gross Domestic Product (GDP) estimated to have grown by 4.3% according to S&P Global, supported by a diversified economic base. Economic indicators also reflected sustained momentum, particularly in business formation, with new business licence issuance rising by 31.5% to 1,789 licences and total active economic licences increasing to 21,938 by year-end. In parallel, Ras Al Khaimah Economic Zone (RAKEZ) continued to play a central role in economic diversification, recording a 44% increase in new company registrations and expanding its business community to over 40,000 entities.

While macroeconomic conditions remained strong, the residential market recorded a moderation in transaction activity in 2025, with total sales volumes declining to approximately 6,600 transactions and total transaction value falling to AED 12.4 billion. This was primarily driven by fewer off-plan launches and a more selective market environment. Despite this moderation, underlying fundamentals remained firm, with prices continuing to rise across both apartments and villas by 13.4% and 9.7% respectively, alongside rental growth of 10.2% for apartments and 8.7% for villas. Supply additions remained limited during the year, with approximately 1,200 units delivered.

Looking ahead to 2026, the residential market outlook remains positive, supported by strong macroeconomic conditions, population growth, and sustained investor and end-user demand. However, the outlook remains subject to external uncertainties, including geopolitical developments in the region, which may influence investor sentiment and inbound demand and will therefore require close monitoring.

Market Snapshot for 2025

- Residential Sales Transactions: ~6,600 (-17.4% Y-on-Y)

- Residential Sales Value: AED 12.4 Billion (-24.7% Y-on-Y)

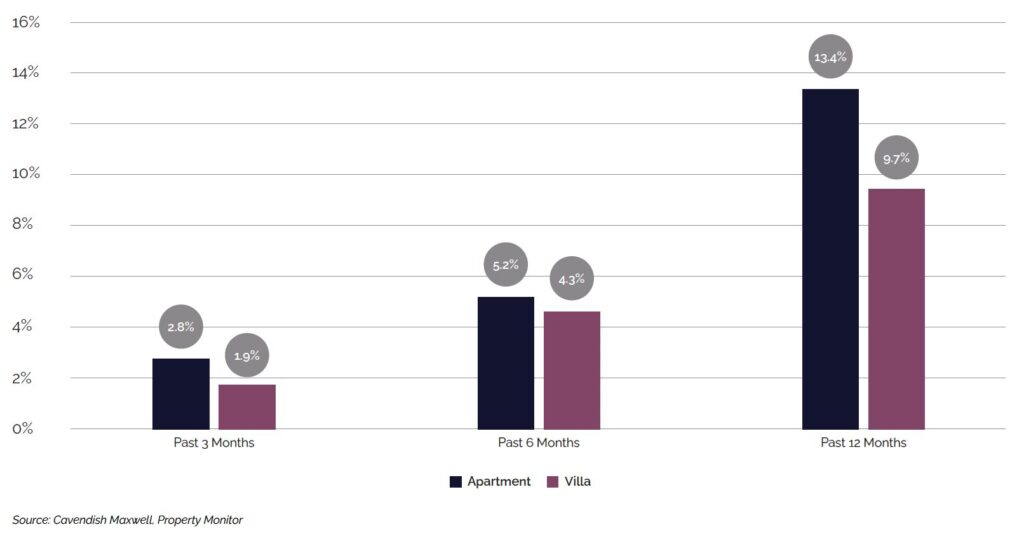

- Apartment Sales Price: +13.4% Y-on-Y

- Villa Sales Price: +9.7% Y-on-Y

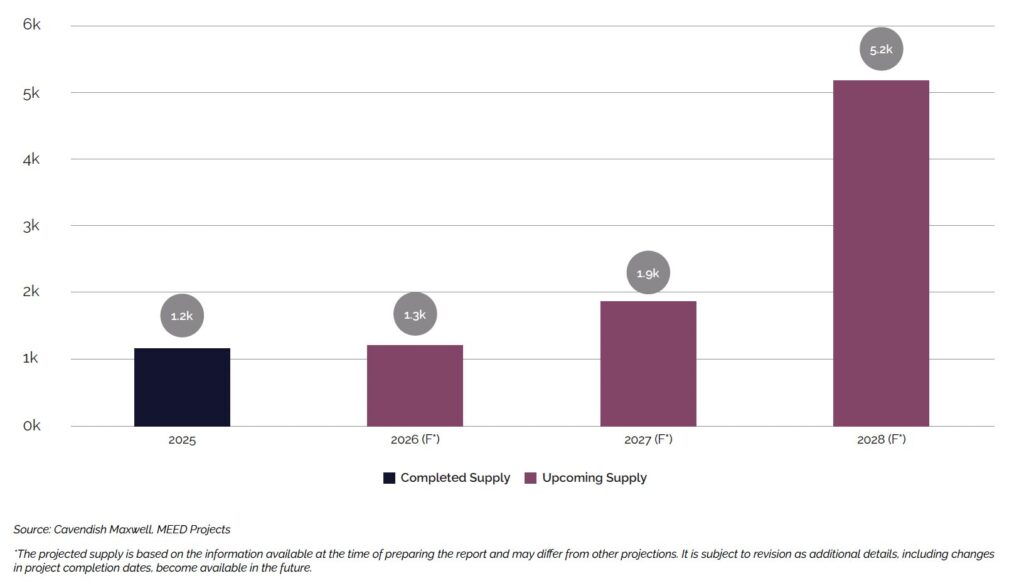

- Residential Supply in 2025:

- Completed: 1,200

- Upcoming in 2026: 1,300

- Upcoming in 2027: 1,900

Macroeconomic Overview and Outlook

Ras Al Khaimah’s macroeconomic fundamentals remained strong in 2025, with GDP estimated to have grown by 4.3%, according to S&P Global, supported by a diversified economic base comprising tourism, construction, real estate activities, manufacturing, and mining. Against this backdrop, economic indicators reflected continued momentum during the year, most notably in business formation and investor sentiment. Ras Al Khaimah recorded a notable improvement in investment attractiveness, with new business licence issuance increasing by 31.5% to 1,789 licences, supported by lower cancellation rates and strengthening confidence in the local business environment. As a result, total active economic licences reached 21,938 by year-end, reflecting annual growth of 5.4%. At the same time, Ras Al Khaimah Economic Zone (RAKEZ) continued to play a key role in driving business expansion, with new company registrations rising by 44% and the total business community surpassing 40,000 entities, supported primarily by services, trading, and e-commerce sectors.

Looking ahead, Ras Al Khaimah’s economic outlook remains positive, supported by its ‘A/A-1’ credit rating with a stable outlook from S&P Global. Performance is expected to be supported by continued investment across tourism, infrastructure, logistics, manufacturing, and real estate, alongside ongoing improvements in connectivity and business formation activity. That said, escalating geopolitical tensions in the region pose a degree of risk to the near-term outlook, with potential implications for investor sentiment, trade flows, and tourism demand that warrant close monitoring.

Sales Transactions

Sales Transactions: By Volume

Ras Al Khaimah’s residential market recorded approximately 6,600 sales transactions in 2025, reflecting a year-on-year decline of 17.4% from 8,000 transactions in 2024. Transaction volumes declined across both segments, with off-plan sales decreasing by 17.2% to around 5,600 transactions, primarily due to a lower number of new project launches compared to the previous year. Ready property transactions also fell by 18.7% to approximately 1,000 transactions. Despite the overall contraction, off-plan properties continued to dominate market activity, accounting for around 85.1% of total sales, broadly consistent with the previous year.

![]()

Ras Al Khaimah’s residential market is maturing with diverse buyers, driven by strategic development and infrastructure investment. As the pipeline expands, balancing supply and demand will be crucial for market sustainability. Project delivery, pricing discipline, and tourism growth will define performance and strengthen long-term residential demand.

Yousir Habib

Associate Director, Commercial Valuation

Sales Transactions: By Value (AED Billions)

In 2025, total sales transaction value in Ras Al Khaimah reached AED 12.4 billion, representing a year-on-year decline of 24.7% from AED 16.4 billion in 2024. Off-plan sales accounted for AED 11.2 billion, down 26.5% year-on-year. In contrast, the ready segment recorded a more modest decline, with sales value easing by 1.8% to AED 1.2 bill ion. In terms of ticket prices, average off-plan prices stood at AED 1.98 million, compared to AED 1.16 million for ready transactions.

![]()

Residential Supply

Ras Al Khaimah’s residential supply grew modestly in 2025, with approximately 1,200 units delivered during the year. Looking ahead, the pipeline accelerates considerably, with 1,300 units projected for completion in 2026, rising to 1,900 units in 2027, before a significant step-up to 5,200 units in 2028. As the pipeline builds, absorption will remain a key consideration, with outcomes largely dependent on the Emirate’s ability to attract and retain residents, alongside continued enhancement of infrastructure, connectivity, and community amenities.

Sales Price Change (%)

Apartment sales prices in Ras Al Khaimah maintained a strong upward trajectory in 2025, increasing by 13.4% year-on-year. Villa prices also recorded growth, rising by 9.7%, reflecting strong demand across both segments. This performance was supported by continued interest from end-users and investors, driven by the Emirate’s expanding portfolio of waterfront developments and branded residential projects, an improving lifestyle offering, and competitive pricing relative to other Emirates.

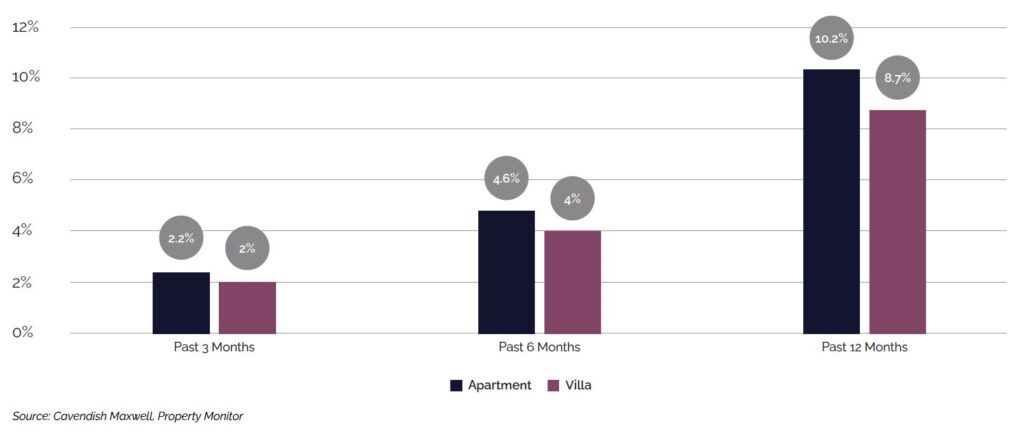

Rental Rate Change (%)

Rental rates in Ras Al Khaimah strengthened in 2025, with apartment rents rising 10.2% year-on-year and villa rents increasing by 8.7%. The upward pressure on rents was largely driven by sustained inward migration, supported by continued business formation and investment activity, alongside a growing resident population, which supported occupier demand across the residential market.

2026 Real Estate Market Outlook

Ras Al Khaimah’s residential market is expected to maintain its positive trajectory over the near to medium term, supported by strong economic fundamentals, a growing population base, and sustained interest from both investors and end-users. While transaction volumes moderated in 2025, reflecting a more selective market environment and fewer off-plan launches, this normalisation has not materially weakened underlying demand conditions, with both sales prices and rental rates continuing to appreciate across the apartment and villa segments throughout the year.

On the supply side, the pipeline over the next two years remains manageable, with approximately 1,300 units scheduled for completion in 2026 and a further 1,900 units in 2027. This provides scope for the market to absorb incoming stock in an orderly manner ahead of a more substantial delivery phase in 2028. The anticipated opening of Wynn Al Marjan Island is also expected to act as a key demand catalyst, with the potential to support tourism inflows, stimulate employment creation, and generate additional housing demand over the medium term.

While the overall outlook for 2026 remains positive, escalating geopolitical tensions in the region introduce a degree of uncertainty around investor sentiment and inbound demand, which will need to be carefully monitored in the period ahead.