Dubai Retail and Warehouse Market Performance 2025

Executive Summary

Dubai’s retail and warehouse sectors demonstrated resilience and growth in 2025, supported by strong fundamentals including record tourism, population growth, and rising e-commerce activity. Both sectors, however, faced tightening supply conditions that shaped market dynamics throughout the year.

The retail sector experienced robust growth in 2025, with sales transaction values rising 48.4% year-on-year to AED 4.6 billion, significantly outpacing the 7.6% increase in transaction volumes. Rental activity showed signs of supply constraint, with new leases declining 15.7% whilst renewals strengthened by 6.5%, as tenants prioritised retaining space in prime locations amid limited availability, pushing rental rates 7.1% higher year-on-year.

Dubai’s warehouse segment also maintained strong demand in 2025, though total leasing volumes declined 1.7% year-on-year to approximately 19,100 transactions, driven by a 29.4% drop in new leases. Renewal activity, however, surged 18%, reflecting occupiers’ preference to retain existing space in a supply-constrained environment. Despite lower transaction volumes, total rental values increased 14.2% year-on-year to AED 3.2 billion, whilst rental rates climbed 17.6% on average.

Looking ahead, the performance of both sectors will depend on the stability of key demand drivers, including tourism, population growth, e-commerce activity, and trade, all of which remain subject to evolving regional conditions and will require close monitoring in 2026.

Retail Sales Transactions

Retail sales transactions reached approximately 1,450 in 2025, marking a 7.6% year-on-year increase. While transaction volumes were split almost evenly between off-plan and ready properties, the off-plan segment gained significant momentum in recent years, with volumes surging 834.2% since 2021.

The true strength of the market, however, was reflected in transaction values. Total sales value rose sharply to approximately AED 4.6 billion, up 48.4% compared to 2024. This growth, which significantly outpaced volume growth, signalled that buyers were transacting at higher price points. Off-plan properties led this trend, generating AED 2.9 billion in sales and capturing 63.4% of total value, compared to AED 1.7 billion or 36.6% for ready assets.

The widening gap between volume and value growth revealed two key market dynamics: price appreciation and a clear shift towards higher ticket price transactions, rather than simply an increase in transaction volume, reflecting strong investor confidence in the retail sector.

Sales Transactions – By Volume

![]()

Dubai’s retail landscape remains fundamentally stable, yet the path forward is more nuanced. While occupancy levels remain healthy so far, the sector’s performance will ultimately depend on stability in key demand drivers, particularly tourism and consumer sentiment, which could be affected by broader regional developments.

Vidhi Shah

Director, Head of Commercial Valuation

Sales Transactions – By Value (AED Billions)

![]()

Retail Rental Transactions

On the rental front, overall rental contracts declined slightly in 2025, driven primarily by a 15.7% drop in new leases amid limited availability of quality retail space. Renewals, however, strengthened considerably, rising 6.5% from 2024.

With prime, high-footfall locations in short supply and rental rates trending upwards, tenants increasingly opted to renew existing agreements rather than risk relocating to less competitive locations. This shift was further evidenced by the increase in the average rental ticket prices, with new contracts averaging 14.2% higher, while renewals only increased by 4%.

Rental Transactions – By Volume

![]()

Retail Rental Performance

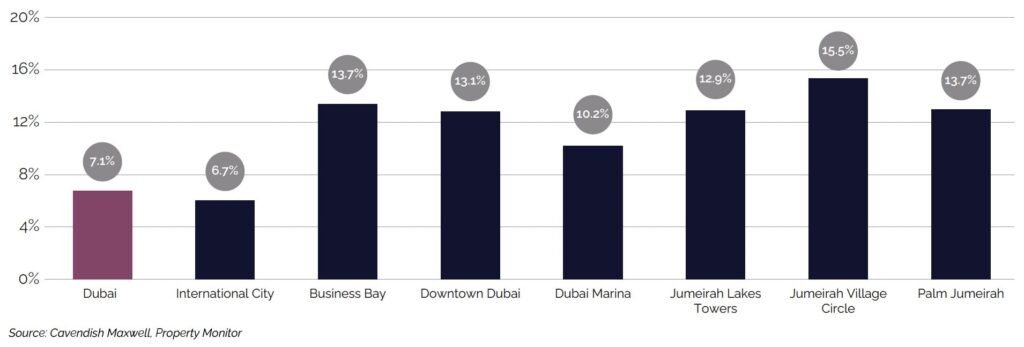

Retail rental rates across Dubai rose 7.1% year-on-year in 2025, driven by growth in community retail and steady performance across retail destinations. Jumeirah Village Circle (JVC) recorded the highest rental growth at 15.5% year-on-year, fuelled by rapid population inflows that strengthened retail demand. Business Bay, Palm Jumeirah, and Downtown Dubai also experienced notable increases, supported by high footfall and more affluent consumer catchments.

The continued rise in rental rates reflects a persistent supply-demand imbalance, with limited availability of quality retail space meeting robust tenant demand. This dynamic was further reinforced by Dubai’s population growth and record tourism levels, both of which continued to support consumer spending across the Emirate.

Rental Rates – Year-on-Year Change (%)

Warehouse Rental Transactions

Warehouse leasing activity softened in 2025, with total contracts declining by 1.7% year-on-year to approximately 19,100 transactions, primarily driven by a 29.4% drop in new leases. In contrast, renewal activity strengthened, rising by 18% year-on-year, reflecting a clear preference among occupiers to retain existing space rather than relocate. This trend highlighted a supply-constrained environment, where limited availability of suitable facilities made relocation increasingly challenging, prompting tenants to prioritise renewals even as rental rates continued to rise across the city. Despite the decline in overall leasing volumes, total rental value increased by 14.2% year-on-year to AED 3.2 billion.

Warehouse Rental Transactions – By Volume

![]()

Warehouse Rental Transactions: by Unit Size

Warehouse rental activity in 2025 was largely concentrated in mid-sized units, with the 2,001–5,000 sq. ft. segment accounting for 51.8% of total transactions. This was driven by strong demand from SMEs, trading companies, and e-commerce businesses seeking functional storage space without committing to larger industrial footprints.

Larger units also represented a notable share of activity, with transactions above 10,000 sq. ft. accounting for 19.5% of the total, primarily driven by bigger occupiers such as logistics operators and manufacturers.

Rental Transactions by Unit Size (%)

![]()

The warehouse sector has demonstrated continued strength, supported by robust e-commerce activity and sustained trade flows. Demand for modern logistics and warehouse facilities remains firm; however, forward visibility is relatively limited. Occupiers are increasingly adopting a strategic approach to space utilisation, reflecting broader economic uncertainties and the need for operational flexibility. We are closely monitoring these trends to assess their potential implications for the warehouse sector, particularly heading into 2026.

Pawan Agrawal

Associate, Commercial Valuation

Warehouse Rental Performance

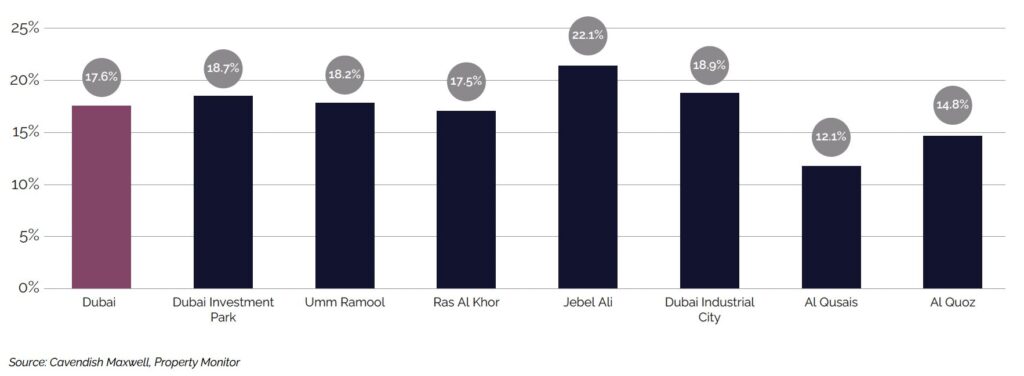

Strong demand and high occupancy levels drove Dubai’s warehouse rental rates up by 17.6% over the past year, though growth varied significantly across submarkets, with increases ranging from 12% to 22%. Jebel Ali led with a 22.1% rise, driven by demand from businesses requiring large-scale, port-adjacent logistics space. Dubai Industrial City followed at 18.9%, reinforcing its position as a dedicated logistics and manufacturing hub, supported by its proximity to Al Maktoum International Airport (DWC), which prompted businesses to secure space early ahead of the airport’s ongoing expansion. Dubai Investment Park recorded 18.7% growth, benefiting from its strategic location near major road networks. Meanwhile, more established areas such as Al Quoz and Al Qusais experienced more moderate increases of 14.8% and 12.1%, respectively.

Rental Rates – Year-on-Year Change (%)

Market Outlook

Dubai’s retail sector closed 2025 on a strong note, supported by 19.6 million international visitors and a growing resident population, both of which drove higher footfall and consumer spending, supporting retailer performance. Occupancy levels remained elevated throughout the year, whilst rental rates across key retail corridors increased steadily, signalling tightening supply conditions in prime locations. Looking ahead, the retail landscape is expected to expand in 2026, supported by a pipeline of community- centric developments. Projects such as Dubai Square, Ghaf Woods Mall, Sobha Mall, Liwan Mall, Villa Square, and South Bay Mall are set to add to the market, reflecting a broader shift towards more localised retail provision that prioritises proximity and convenience over traditional destination-led formats. However, the timing and phasing of new supply will be influenced by broader market conditions, which may result in adjustments to development schedules. At the same time, the sector is increasingly adopting emerging technologies as operators place greater emphasis on enhancing customer engagement and sustaining footfall, a trend likely to gain momentum in 2026.

Alongside the strong performance of the retail sector, demand across Dubai’s warehousing segment also remained robust in 2025, supported by rising e-commerce activity and sustained interest from both domestic and international businesses. Occupiers continued to prioritise modern, high-spec facilities, with greater emphasis on automation, operational efficiency, and specialised infrastructure. This trend is expected to continue into 2026 as occupier requirements become more sophisticated. Concurrently, government-led initiatives such as the UAE Global Centre of Trade programme, which seeks to attract leading international trading companies to establish operations across the country, are expected to provide further support to demand in Dubai.

Whilst both sectors demonstrated growth through 2025, the outlook for 2026 remains subject to a number of market considerations. Tourism, population growth, e-commerce activity, and trade activity have historically supported demand, but the stability of these drivers will be influenced by evolving regional conditions. Within the retail sector, fluctuations in tourism arrivals or shifts in consumer confidence and discretionary spending could influence demand. Similarly, in the warehousing segment, changes in trade flows or supply chain dynamics could impact demand for warehouse space. Nevertheless, Dubai’s track record of policy agility and ongoing investment aligned with the D33 economic agenda is expected to support overall market resilience.