Dubai Retail and Warehouse Market Performance Q1 2026

Executive Summary

Dubai’s retail and warehouse sectors entered 2026 with positive market fundamentals, supported by population growth, economic expansion and resilient occupier demand. While activity in Q1 was influenced by the timing of Ramadan and heightened regional uncertainty, overall market performance remained stable, with both sectors demonstrating underlying resilience despite a moderation in transactional activity.

Retail performance was characterised by strong growth in sales activity, with transaction volumes rising 51.6% year-on-year and values increasing 171% to AED 2.1 billion, supported by higher-value transactions and price appreciation. However, leasing activity softened, with total contracts declining 7.2% year-on-year, reflecting an ongoing preference for renewals over new leasing. Despite this, retail rental rates increased 6.4% year-on-year, with performance increasingly differentiated by location, as community- led retail assets remained resilient while tourism-linked destinations faced a more uncertain environment.

The warehouse sector reflected stable structural dynamics, with leasing activity declining 7.3% year-on-year due to weaker new leasing demand, while renewals increased as occupiers retained existing space. Activity remained concentrated in small to mid-sized units, alongside sustained demand for larger logistics-oriented space. Rental rates rose 16.1% year-on-year, supported by constrained availability across key industrial locations. Looking ahead, while near-term conditions may remain influenced by regional uncertainty, underlying demand drivers, including Dubai’s role as a regional trade hub and ongoing economic diversification, are expected to support long-term market stability.

Retail Sales Transactions: Volume

Retail sales transactions reached approximately 485 in Q1 2026, representing a 51.6% year-on-year increase. Compared to Q4 2025, however, activity declined marginally by 3.8%, broadly in line with the seasonal slowdown typically observed during the first quarter. Growth was primarily driven by the off-plan segment, where transactions increased 75.2% year-on-year, while the ready market also recorded positive momentum, rising 32% over the same period.

On a monthly basis, activity increased from 139 transactions in January to 196 in February before moderating to 150 in March. The slowdown was largely driven by weaker ready market activity, which declined 35.9% year-on-year in March. In contrast, off-plan transactions continued to strengthen, increasing by 194.6% over the same period. However, March figures should be interpreted with caution given the registration lag typically associated with off-plan sales. Activity over the coming months should provide greater clarity on underlying demand trends.

Sales Transactions – By Volume

![]()

Retail Sales Transactions: Value

Beyond sales volumes, total retail sales value reached AED 2.1 billion in Q1 2026, representing a 171% year-on-year increase. Compared to Q4 2025, however, it declined marginally by 2.4%. Off-plan transactions generated AED 1.3 billion, accounting for 62% of total value and increasing by 224.8% year-on-year, while ready transactions contributed AED 0.8 billion, up 113.5% over the same period. The stronger growth in sales value relative to transaction volumes (+51.6%) reflects both price appreciation and a shift towards higher-value assets. As a result, average transaction value increased to AED 4.3 million in Q1 2026, up from AED 2.4 million in Q1 2025.

Sales Transactions – By Value (AED Billions)

![]()

Retail Rental Transactions

Retail leasing activity recorded approximately 19,800 contracts in Q1 2026, representing a 7.2% decline compared to Q1 2025. The market remained heavily driven by renewals, which accounted for 82.1% of all contracts and increased by 1.3% year-on-year. In contrast, new leasing activity declined by 33.2%, suggesting occupiers preferred to retain existing locations amid a more uncertain operating environment.

On a monthly basis, activity moderated to approximately 4,600 contracts in March, down 14.7% year-on-year. The decline was primarily driven by weaker new leasing demand, with new contracts falling 40.8% year-on-year. It is worth noting, however, that leasing activity had already been moderating prior to the onset of regional uncertainty, suggesting recent developments have accelerated an existing trend rather than initiated it.

Rental Transactions – By Volume

![]()

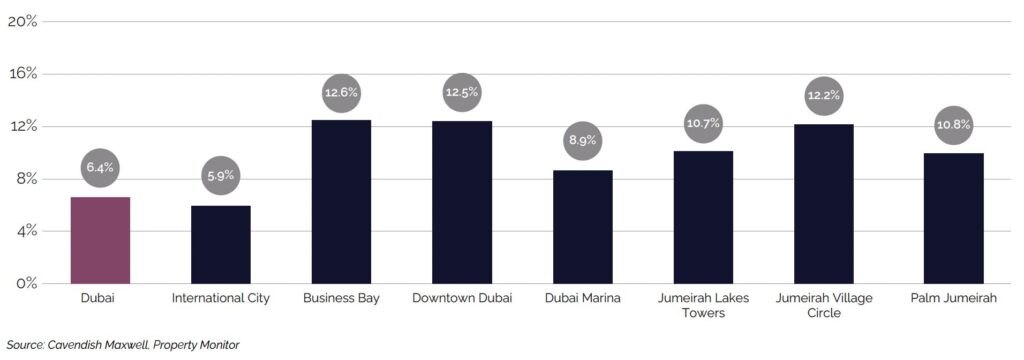

Retail Rental Performance

Retail rental rates in Dubai continued to strengthen in Q1 2026, rising 6.4% year-on-year, supported by the emirate’s expanding population and sustained demand across established residential catchments. While the pace of rental growth may vary over the coming quarters, performance is likely to become increasingly differentiated by location quality, with occupier demand remaining concentrated in well-located assets with strong footfall, while landlords in more competitive locations may face greater pressure to attract and retain tenants.

Rental Rates – Year-on-Year Change (%)

Warehouse Rental Transactions

Warehouse leasing activity recorded approximately 5,800 contracts in Q1 2026, representing a 7.3% year-on-year decline. The market remained heavily driven by renewals, which accounted for 83.7% of all contracts and increased by 14.7% year-on-year to approximately 4,800 contracts. In contrast, new leasing activity declined by 53.4% to 900 contracts, reflecting both reduced expansion activity from existing occupiers and a softer inflow of new market entrants. On a monthly basis, activity in March declined by 11.3% year-on-year. The slowdown was primarily driven by weaker new leasing demand, with new contracts falling by 66.3% year-on-year, while renewal contracts continued to grow, increasing by 28.7% over the same period.

Rental Transactions – By Volume

![]()

Rental Transactions: by Unit Size

Warehouse leasing activity in Q1 2026 was concentrated in small to mid-sized units. Properties ranging from 2,000 to 5,000 sq. ft. accounted for the majority of transactions, representing 51.3% of total activity, highlighting continued demand for smaller, flexible warehouse formats typically associated with SMEs and light industrial users. This was followed by larger units exceeding 10,000 sq.ft., which accounted for 19.8% of transactions, indicating sustained activity in larger warehouse formats typically utilised by logistics and storage operators.

![]()

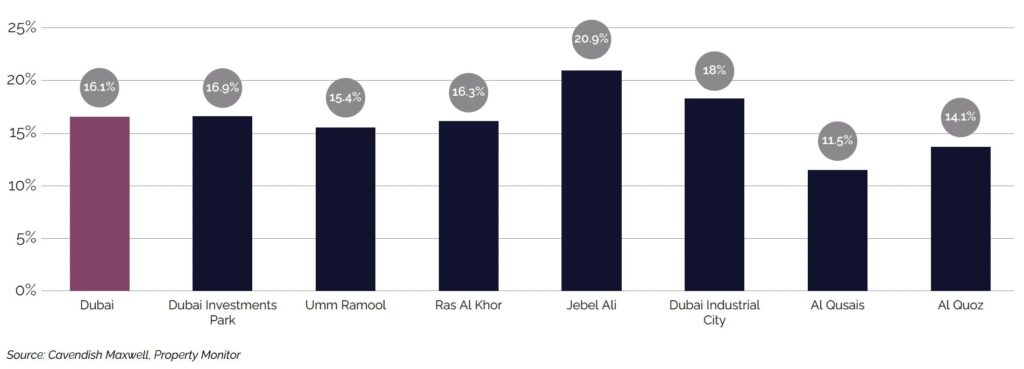

Warehouse Rental Performance

Warehouse rental rates in Dubai continued to strengthen in Q1 2026, rising 16.1% year-on-year, with Jebel Ali recording the strongest growth, followed by Dubai Industrial City, Dubai Investments Park and Ras Al Khor. The sustained upward trajectory reflects constrained availability of quality warehouse space alongside occupier demand for efficient and resilient supply chains, supporting continued interest in well-located assets within key industrial hubs. While broader regional uncertainty may lead to more cautious expansion decisions in the near term, structural requirements for storage and distribution are expected to support demand for quality warehouse space within well-located industrial hubs over the medium-term.

Rental Rates – Year-on-Year Change (%)

Market Outlook

Dubai’s retail and warehouse sectors entered 2026 with supportive market fundamentals, although activity in Q1 was influenced by the timing of Ramadan and heightened regional uncertainty, which weighed on leasing activity towards the end of the quarter.

Within retail, tenant retention remained strong in Q1 2026, with many occupiers opting to renew rather than relocate or expand. Performance is expected to vary by format and location, with community and convenience-led assets likely to remain resilient, while tourism-linked destinations may face a more challenging environment if visitor arrivals and consumer spending soften. As a result, occupiers are expected to remain selective, favouring locations with strong footfall and established catchments.

Dubai’s warehousing sector continued to reflect stable structural dynamics in Q1. Rental rates rose in all areas – the result of limited availability in key locations – and demand for well-positioned space at established industrial hubs is expected to continue. While activity may be influenced by regional conditions, market fundamentals remain supportive, and continued investment under the D33 agenda is likely to mean sustained demand and long-term market performance.

Vidhi Shah

Director, Head of Commercial Valuation

The warehouse sector continues to benefit from Dubai’s position as a regional trade and distribution hub, alongside ongoing investment in logistics and industrial infrastructure. At the same time, increased regional uncertainty may lead some occupiers to adopt a more cautious approach to expansion, potentially weighing on new leasing activity. Demand for well-located warehouse space within established industrial hubs is expected to remain supported by underlying storage and distribution requirements, which should continue to support rental performance.

Overall, while activity may remain influenced by evolving regional conditions, market fundamentals remain supportive. Continued investment under the D33 agenda, together with the Dubai Government’s support measures, is expected to reinforce business confidence and support long-term market performance.