Abu Dhabi Residential Market Performance H1 2025

Executive Summary

Abu Dhabi’s economy demonstrated strong momentum in H1’2025, driven by robust non-oil trade, foreign investment, and high business confidence. Non-oil foreign trade rose 34.7% to AED 195.4 billion. Business sentiment remained positive, with Abu Dhabi Chamber membership exceeding 158,000 companies and foreign net investment on the Abu Dhabi Securities Exchange (ADX) nearly doubling to AED 13.6 billion. The aviation sector supported this growth, handling over 15.8 million passengers, aided by expanded international connectivity. Strategic infrastructure projects, ongoing diversification, and investor-friendly policies strengthened economic activity and attracted skilled talent, providing a solid foundation for the residential market.

Abu Dhabi City’s residential market shifted towards ready properties in H1’2025, with approximately 3,300 transactions recorded, including around 2,300 ready and just over 1,000 off-plan sales. Off-plan activity declined during the period due to limited new launches; however, sources suggest that off-plan transaction volumes are likely to be revised upward, reflecting stronger-than-initially-reported activity. Ready property sales remained strong compared to H1’2024, supported by end-user and investor demand. Residential supply gradually increased, with around 2,400 units delivered in H1’2025 and an additional 10,400 units expected by year-end. Prices and rental rates continued to rise, reflecting constrained supply and steady demand: apartment prices grew 14.4% year-on-year, while villa prices increased 11.1% year-on-year. Apartment rents rose 13.9% year-on-year, with villa rents showing moderate growth.

Looking ahead, the residential market is expected to maintain steady growth through the remainder of 2025, supported by strong buyer demand, ongoing infrastructure development, and the inflow of skilled professionals drawn by new employment opportunities and business creation. Market conditions are likely to continue shaping both sales and rental performance, with demand expected to outpace supply in key segments in the near term.

Market Snapshot for H1 2025

- Sales Transactions: +3,300 (-36.9% Y-on-Y)

- Sales Value: AED 8.9 Billion (-33% Y-on-Y)

- Apartment Sales Price: +14.4% Y-on-Y

- Villa Sales Price: +11.1% Y-on-Y

- Residential Supply in 2025:

- 10,400 (Under-construction)

- 2,400 (Completed)

Macroeconomic Overview and Outlook

According to the latest statistics released by Abu Dhabi Customs, the Emirate’s non-oil foreign trade continued its robust growth in the first half of 2025, rising 34.7% to AED 195.4 billion, up from AED 145 billion during the same period in 2024. Over this period, non-oil exports surged 64%, reaching AED 78.5 billion compared to AED 47.9 billion in H1’2024. Imports increased 15% to AED 80 billion, up from AED 70 billion, while re-exports rose 35%, surpassing AED 36 billion compared to AED 26.6 billion in the first half of 2024.

Business confidence also remained strong, with Abu Dhabi Chamber membership exceeding 158,000 companies, a 4.9% increase that highlights the Emirate’s continued appeal as a business hub. The Abu Dhabi Securities Exchange (ADX) reported a 99.5% surge in foreign net investment, reaching AED 13.6 billion, reflecting growing international investor confidence. The aviation sector further supported this trend, with Abu Dhabi Airports handling over 15.8 million passengers, a 13.1% increase compared to H1’2024, driven by expanded international routes and increased tourism connectivity.

Looking ahead, Abu Dhabi’s economy is expected to maintain its growth momentum, supported by ongoing diversification, strategic infrastructure projects, and a favourable business climate. The Emirate’s resilient economic model, combined with investor-friendly policies and transparent governance, continues to stimulate business creation and job opportunities, attracting skilled talent to the city. This inflow of professionals is likely to support demand in the residential market.

Sales Transactions

Abu Dhabi’s residential market in H1’2025 continued its shift towards ready properties, with approximately 3,300 sales transactions, including around 2,300 ready sales and just over 1,000 off-plan sales. Off-plan activity fell in the first half of 2025, declining by 49.5% from H2’2024 and by 69.9% from H1’2024, as fewer new project launches left limited inventory for buyers. Although off-plan volumes in Q1 and Q2 2025 were below previous quarters, Q2 did see a modest uptick in activity. According to other sources, off-plan transaction numbers are expected to be revised upward, potentially increasing total H1’2025 sales activity.

This relative scarcity of off-plan options redirected demand towards ready properties, allowing them to grow their share in H1’2025. While the volume of ready sales was lower than in H2’2024, it remained 26.9% higher year on year, highlighting the strength of end-user and investor demand in the absence of fresh off-plan supply.

Abu Dhabi City Transactions – By Volume

Source: Quanta, Cavendish Maxwell

In terms of residential sales value, H1’2025 saw transactional values reach approximately AED 8.9 billion, marking a 33% decline compared to the same period last year, largely due to subdued off-plan activity. However, while the number of ready property transactions fell compared with H2’2024, their total sales value increased. Over the same period, the average transaction price for ready properties rose from AED 2.1 million to AED 2.5 million.

Abu Dhabi City Transactions – By Value (AED)

Source: Quanta, Cavendish Maxwell

Sales Transactions by Property Type: Apartments

While apartments continued to dominate Abu Dhabi City’s residential sales in H1’2025, their market share eased from 76.4% in H1’2024 to 73.3%, reflecting a modest shift in buyer activity. Over the same period, transaction volumes fell by 27.8% compared with H2’2024 and 39.4% year-on-year, driven largely by a slowdown in off-plan sales amid fewer project launches. Ready transactions, although lower than in H2’2024, rose 14.1% compared with H1’2024, supported by strong end-user and investor demand, reflecting the market’s growing reliance on completed homes amid constrained off-plan supply.

Abu Dhabi City Apartment Transactions – By Volume

Source: Quanta, Cavendish Maxwell

Sales Transactions by Property Type: Villas and Townhouses

Despite a decline in off-plan villa and townhouse transactions compared with H2’2024 and H1’2024, ready villas and townhouses continued to perform strongly, with volumes rising 13.3% from H2’2024 and 72.2% year-on-year, reaching their highest levels since 2021. This growth was driven by buyers seeking larger, family-oriented homes with amenities. Investors, meanwhile, were attracted not only by the yields offered by villas and townhouses but also by potential long-term capital appreciation.

Abu Dhabi City Villa/Townhouse Transactions – By Volume

Source: Quanta, Cavendish Maxwell

Mortgage Transactions

In H1’2025, Abu Dhabi City registered around 1,700 mortgage transactions, marking a 29.2% decline from H2’2024 and a 26.0% drop year-on-year. This contraction was driven primarily by a fall in apartment mortgages, which fell by nearly half compared with the previous half-year. While villa and townhouse mortgage transactions also declined year-on-year, the drop was far less pronounced and even showed a slight increase compared with H2’2024.

Abu Dhabi City Mortgage Transactions – By Volume

Source: Quanta, Cavendish Maxwell

The total value of residential mortgage transactions in Abu Dhabi City reached AED 3.5 billion in H1’2025, with villas and townhouses contributing AED 2.5 billion. Although overall mortgage values fell 11.6% compared with H2’2024, they rose 11.8% year-on-year, supported by a sharp 47.4% annual increase in villa and townhouse mortgage values. This rise offset the steep 31.1% year-on-year decline in apartment mortgage values.

Abu Dhabi City Mortgage Transactions – By Value (AED)

Source: Quanta, Cavendish Maxwell

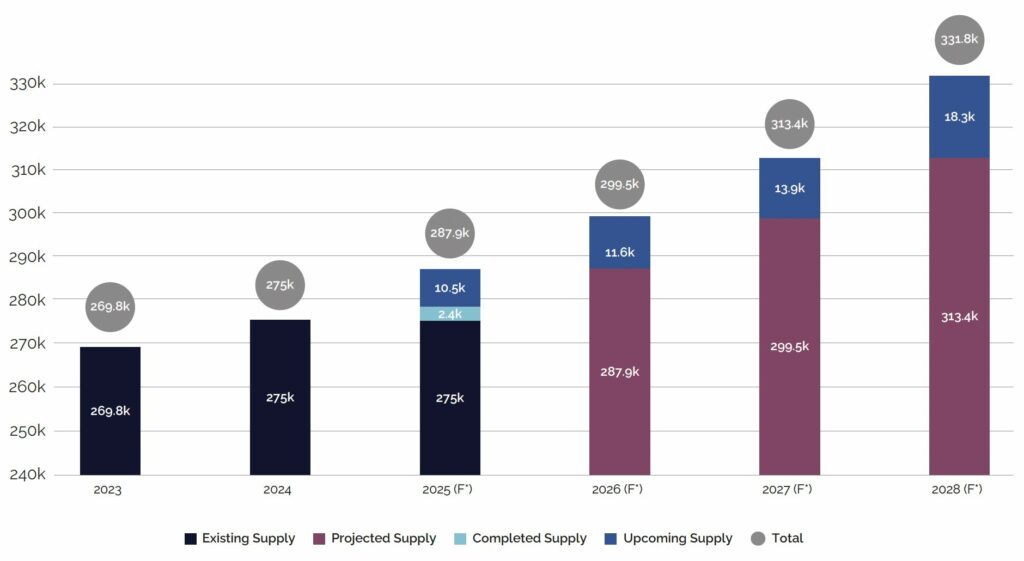

Existing and Future Supply

Residential supply in Abu Dhabi City gradually rose, with around 2,400 units delivered in 2025. The development pipeline is expected to pick up pace, with approximately 10,400 units projected for completion by year-end and over 11,000 units scheduled for delivery in 2026. However, on-the-ground deliveries are expected to progress more slowly than planned, keeping supply below near-term demand.

Concurrently, the Government’s Vision 2030 economic diversification strategy, combined with steady population growth driven by international migration, continues to fuel robust demand for family-oriented, quality homes with modern amenities. Furthermore, strengthening economic conditions across the UAE and broader GCC region are bolstering investment appetite, providing additional support for residential property demand.

Abu Dhabi Supply – Number of Units

Source: MEED Projects, Cavendish Maxwell

*The projected supply is based on the information available at the time of preparing the report and may differ from other projections. It is subject to revision as additional details, including changes in project completion dates, become available in the future.

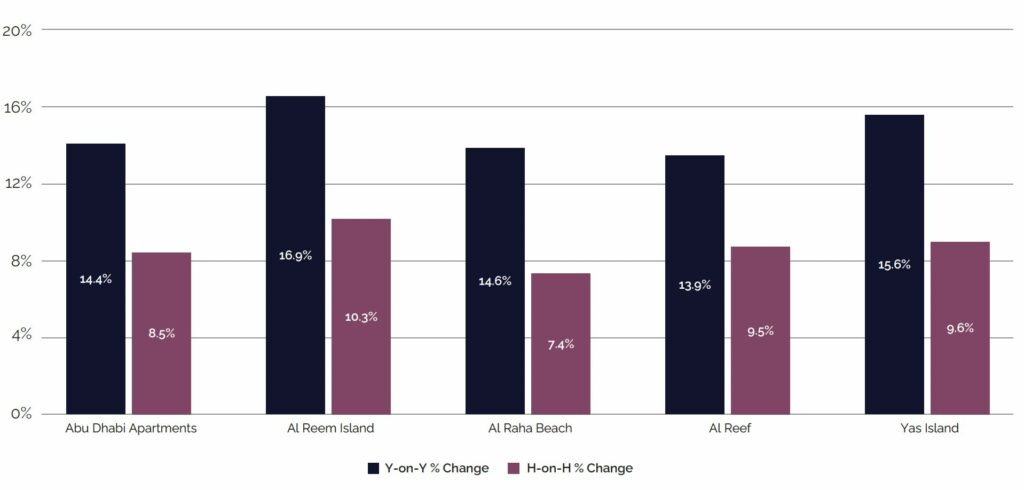

Abu Dhabi Sales Price Change

While overall apartment transactions in Abu Dhabi softened in H1’2025, citywide and submarket prices continued to rise, with citywide prices up 8.5% compared to H2’2024 and 14.4% year-on-year. This trend reflects a supply-constrained market, where limited availability of desirable units is putting upward pressure on prices. Buyers are increasingly focusing on high-quality, well-located apartments, indicating that market performance varies by location and quality and showing that price resilience is largely driven by scarce, in-demand stock.

Abu Dhabi Apartment Sales Price Change (%)

Source: DARI (Abu Dhabi Real Estate Centre), Quanta, Cavendish Maxwell

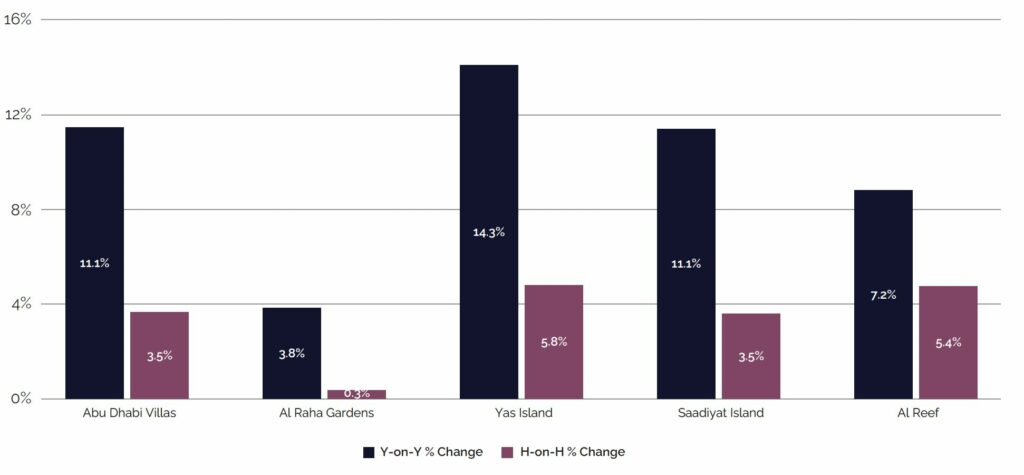

Villa prices in Abu Dhabi continued to rise in H1’2025, albeit at a more moderate pace compared to apartments. At the citywide level, prices increased by 3.5% half-on-half and 11.1% year-on-year, reflecting steady demand across the segment.

Abu Dhabi Villa Sales Price Change (%)

Source: DARI (Abu Dhabi Real Estate Centre), Quanta, Cavendish Maxwell

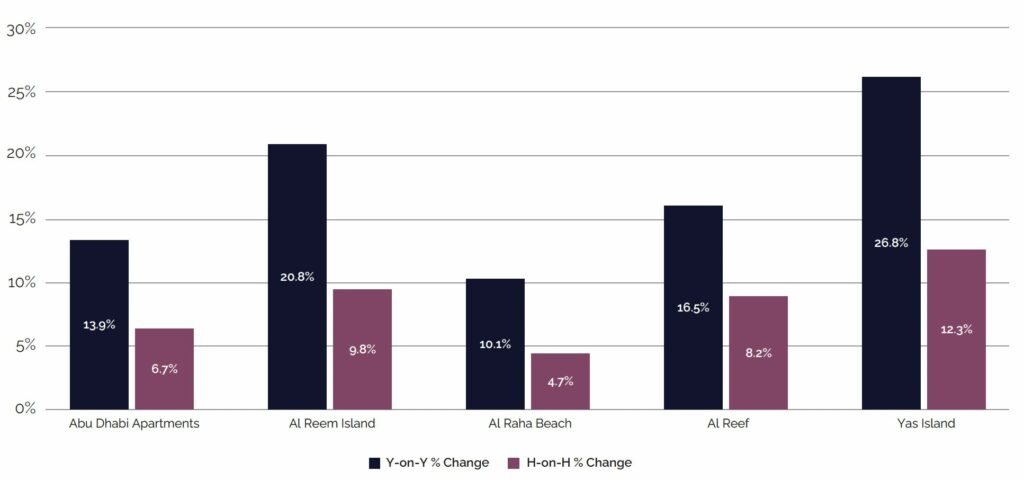

Abu Dhabi Rental Rate Change

As Abu Dhabi’s population continues to grow and inward migration persists, rental rates in the city increased by 6.7% half-on-half and 13.9% year-on-year. However, growth varied across submarkets, with some communities recording single-digit increases while others experienced double-digit annual rental growth. These variations are driven by market dynamics, influenced by factors such as location, property quality, and community amenities, highlighting that tenants continue to be willing to pay a premium in certain segments of the market.

Abu Dhabi Apartment Rental Rate Change (%)

Source: DARI (Abu Dhabi Real Estate Centre), Quanta, Cavendish Maxwell

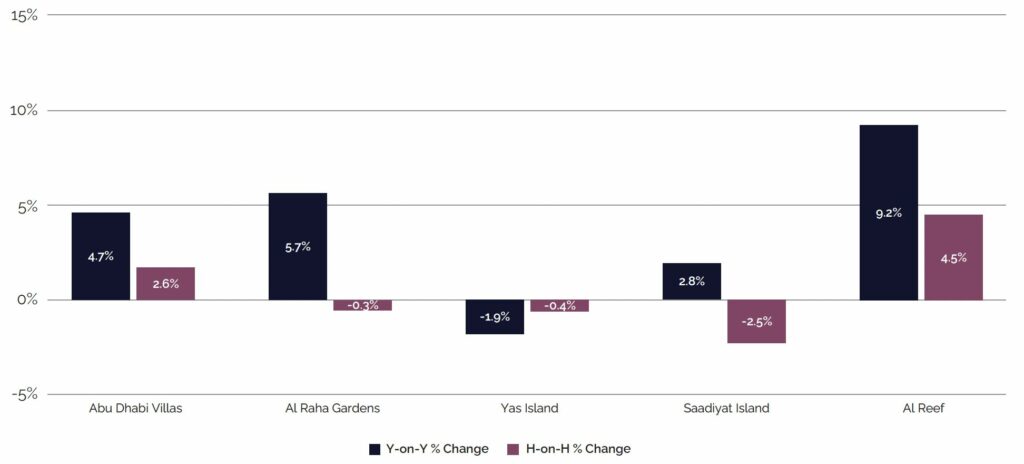

Villa rental rates in Abu Dhabi showed moderate growth in H1’2025, with citywide rents rising 2.6% half-on-half and 4.7% year-on-year. Performance across submarkets was mixed, reflecting diverse demand dynamics: areas such as Al Reef experienced the strongest growth, while others, including Yas Island, saw declines compared to H1’2024.

Abu Dhabi Villa Rental Rate Change (%)

Source: DARI (Abu Dhabi Real Estate Centre), Quanta, Cavendish Maxwell

2025 Real Estate Market Outlook

Abu Dhabi City’s residential market began 2025 on a softer note, with sales activity easing across both ready and off-plan segments compared to H2’2024. While the ready segment recorded an uptick from the same period last year, off-plan sales declined year-on-year, largely due to limited new launches and seasonal factors. However, other sources suggest that off-plan transaction volumes are likely to be revised upward, reflecting stronger-than-initially-reported activity. Ready transactions are expected to remain steady in H2’2025, supported by strong demand across buyer groups, while the performance of the off-plan segment will depend on the scale and timing of upcoming project launches. Early indicators suggest that off-plan activity could gain momentum later in the year, provided new launches materialise.

In terms of supply, approximately 10,400 residential units are expected to be delivered over the remainder of 2025. Absorption is likely to vary across segments, with prime and well-located units attracting stronger demand, while mid-tier or peripheral projects may see slower uptake. Overall, prevailing market conditions will continue to shape both sales and rental performance, with growth expected to continue in the near term.

The first half of 2025 has presented a nuanced picture of the real estate market. While overall activity has moderated compared to the same period in 2024, demand for completed projects remains robust. This sustained interest has driven continued price appreciation across both apartment and villa segments, underscoring the resilience of end-user and investor appetite.

A notable trend in H1 has been the reduced volume of new project launches. However, this is expected to shift in late H1’2025 and early H2’2025, with several large-scale off-plan developments anticipated to enter the market. These upcoming launches are likely to reinvigorate supply and stimulate broader market engagement.

Key developers such as Aldar and Modon are expected to make continued market moves in the coming months, complemented by a growing presence of smaller private developers initiating new projects around the H1/H2 threshold.

Together, these dynamics set a strong foundation for H2 2025, with promising prospects across both off-plan and completed segments. The market continues to show depth and adaptability, positioning itself well for sustained growth in the months ahead.

Andrew Laver

Associate Director, Commercial Valuation – Abu Dhabi