Dubai Residential Market Performance 2024

Macroeconomic Overview and Outlook

Macroeconomic Overview

The Gulf’s macroeconomic performance remains impressive, with the UAE leading the charge. While macroeconomic cycles have not disappeared, investors can take confidence in the fact that their impact has been significantly less in the past decades. The positive macro signals correlated strongly with exceptional real estate performance.

Apart from high rental growth, 2024 saw inflation and debt under control in Dubai and the UAE, with fiscal policy delivering a surplus that was supported by carefully crafted taxation policy, as well as interest rate reductions from the US Federal Reserve. Dubai also achieved its third successive year as the world’s leading greenfield FDI destination, capturing no less than 6.2% of global investment, while the population surpassed the 3 million threshold for the first time.

The result was real economic growth of 3.1% for Jan-Sep 2024. Sectors such as tourism, transportation and storage, and financial services all benefitted from regional growth, surpassing previous records and playing a prominent role in the overall performance. Each sector contributed significant synergy to the local real estate market, which, in turn, supported Dubai’s macroeconomic success and it’s continued rise in the global city rankings.

Macroeconomic Outlook

At the macro level, 2025 is expected to follow suit. Driven by falling interest rates, ongoing government reform, increased project spending by both the government and private sector, and the prospect of improved geopolitical conditions, Oxford Economics predicts that the region will achieve 3.6% overall growth, almost 30% higher than the global average, with Dubai and the UAE once again leading the way.

While this impressive figure conceals the expected continued success of sector diversification, services and manufacturing are predicted to outpace the resource sector for yet another year. The important question facing investors in Dubai is whether the macroeconomic and real estate cycles, which run on different time cycles, have now reached a point of short-term divergence.

Dubai Residential Market Performance

Dubai’s residential real estate market showcased exceptional performance throughout 2024, setting records in both transaction volume and value. This exceptional growth could be attributed to several factors, such as geopolitical conditions, strong macroeconomic trends, robust population growth, world-class regulatory environment for business, and rising foreign investment.

In this report, we explore the key drivers fuelling this momentum, analyse trends in property prices and sales volumes, and examine the outlook for Dubai’s residential sector.

Price Appreciation and Market Stability

By the end of 2024, Dubai’s residential real estate market had grown by at least 17% year-on-year. However, price appreciation has begun to slow – a trend that was anticipated, given that the rate of price growth in this cycle has been nearly double that of the previous cycle. The monthly rate of growth has now moderated to just over 1%, representing a more stable and sustainable figure.

Looking at past market cycles, regulators, developers and investors are acting to avoid runaway growth, where month-on-month increases of 2% to 2.5% persisted. If such growth continues in 2025, it could threaten the market’s sustainability, as seen in previous cycles.

Record Transactions and Strong Momentum

The impact of continued, stable price appreciation has been significant on sales transactions, with record-breaking activity almost every month. In 2024, total residential sales volume reached 169,000 transactions, marking a 42% increase compared to the previous year.

Market Performance and Leading Developers

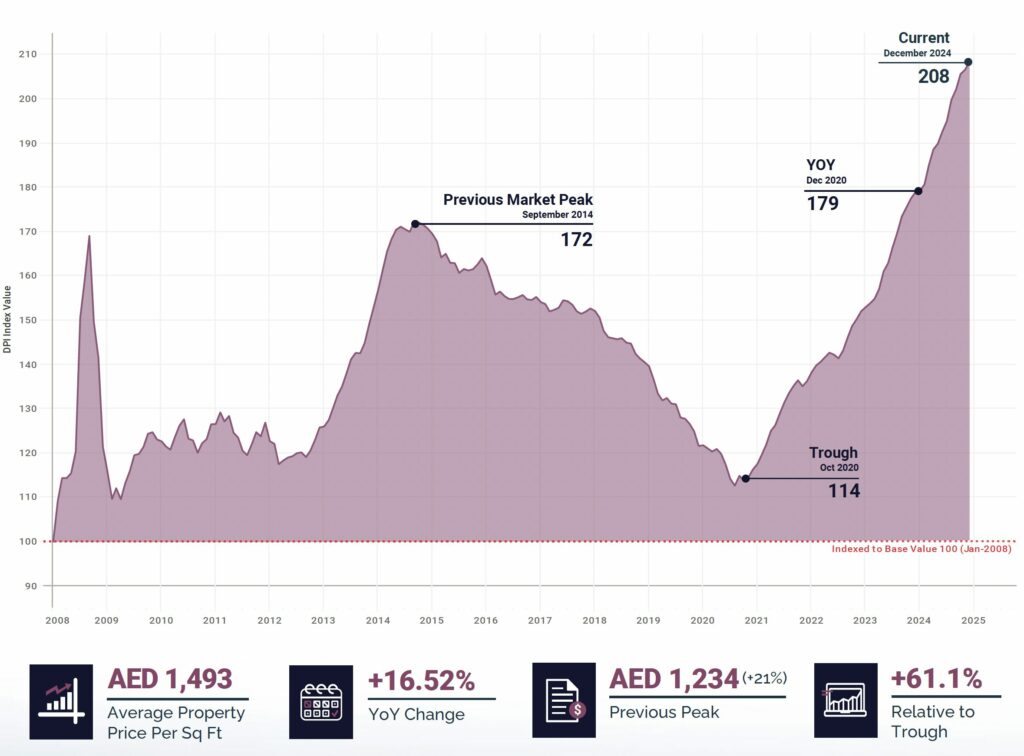

Dubai’s residential market continued its upward trajectory, with the property index reaching a new high of 208 in December 2024. Prices have now risen to AED 1,493 per square foot, reflecting a 90.2% increase from the market low of April 2009.

The year ended on a consistent note, with December recording a month-on-month price increase of 0.9%, extending the streak to 47 consecutive months of gains. On a quarterly basis, prices surged by 3.1%, while year-over-year growth remained robust at 16.5%.

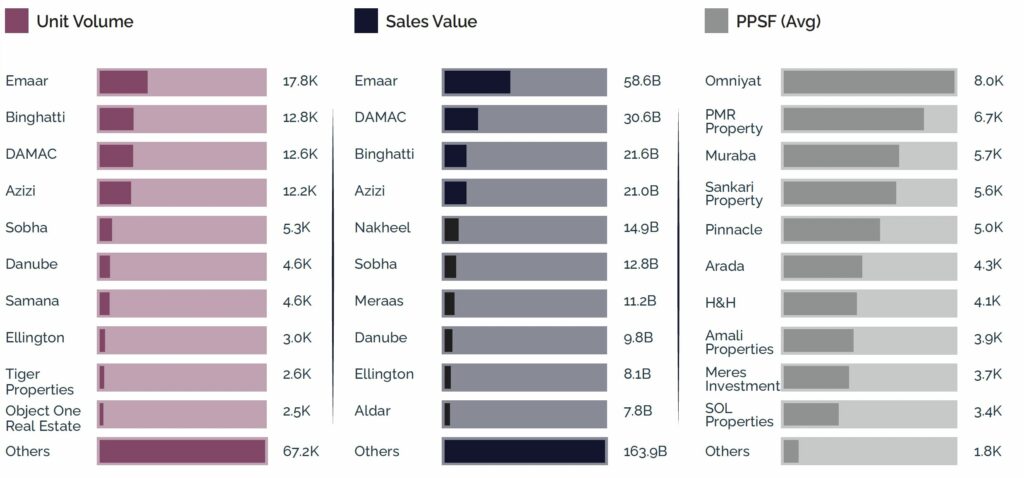

Leading developers continue to drive this growth. Emaar, DAMAC, and Sobha Realty secured the top three spots for the year, with Emaar holding the largest market share at 15.8%, closing approximately 17,250 transactions. DAMAC followed with a 9.7% market share and 10,500 transactions, while Sobha Realty captured 8.3% of the market with 9,100 transactions. These figures highlight the continued strength and competitive nature of Dubai’s real estate sector.

Top 10 Real Estate Developers by Transactional Volume

| Developers | Rank-2024 | Rank-2023 | Rank change from 2023 |

| Emaar | 1 | 1 | – |

| Damac Properties | 2 | 2 | – |

| Sobha Group | 3 | 3 | – |

| Azizi | 4 | 6 | +2 |

| Binghatti | 5 | 5 | – |

| Danube Properties | 6 | 4 | -2 |

| Samana Developers | 7 | 11 | +4 |

| Aldar Properties* | 8 | NA | NA |

| Meraas | 9 | 8 | -1 |

| Ellington Properties | 10 | 10 | – |

*Aldar Properties had no sales transactions in Dubai in 2023; therefore, the developer was not ranked that year

Source: Property Monitor

Luxury Market Activity

The luxury property market in Dubai (properties over AED 20 million) remains exceptionally strong, with record-breaking sales continuing.

In December 2024, the most expensive property sold was a luxury villa in Palm Jumeirah for AED 200 million, while the priciest property of the year was an AED 275 million penthouse at One Palm Jumeirah.

Despite limited inventory in the ultra-high-end segment (properties over AED 50 million), the top-end of the market continued to experience strong transaction activity. These high-value transactions highlight Dubai’s status as a premier destination for exclusive, high-end real estate. At the same time, the substantial growth in the mid-market is driving both prices and sales volumes higher.

Mortgage Market Trends

Mortgage activity grew dramatically during 2024, reflecting the broader rise in sales transactions. The number of registered loans hit an all-time high of 36,600, marking a 30.2% increase compared to 2023. This new height in mortgage activity aligns with recent interest rate easing, making financing more accessible and attractive for buyers. There has also been a surge in bulk mortgage transactions. This increase is likely driven by developers and investors with large portfolios, capitalising on the small rate reduction ahead of their loan maturities. With limited time remaining on their loans, many have chosen to act now.

If interest rates decline by 75 to 100 basis points, with U.S. Federal Reserve signalling two potential reductions in 2025, the UAE Central Bank may follow suit. This could make refinancing an attractive option for many mortgage holders, driving increased market activity and refinancing opportunities.

Additionally, borrowers may also choose to take advantage of higher property valuations to release equity, so further growth in total mortgage value outstanding is to be expected.

Off-Plan Project Launches

The exceptional growth in off-plan sales seen during 2024 underscored the ongoing demand and resilience of Dubai’s property market. Each month witnessed historic transaction levels, signalling a robust investment climate.

The total off-plan transaction volume this year is four times that of pre-COVID levels. This is not now merely a result of pandemic recovery; it reflects a market that was already stable and has been growing since 2022. The current transaction volume is driven by strong international demand, especially from India, China and other Middle Eastern buyers.

Off-plan project launches have been booming in 2024, with nearly 145,000+ new units brought to market, surpassing last year’s total. On average, a new off-plan development is being launched every day, adding around 400 units to the market daily.

These units are being rapidly absorbed, with developers selling the majority within a short time frame. Developers and investors alike are now focused on the average time of holding after first purchase, which has reduced to levels not seen since the last market peak.

Leading five Dubai submarkets – Units delivered in 2024

- Mohammed Bin Rashid City

5,300 units - Jumeirah Village Circle

4,818 units - Business Bay

2,811 units - Al Furjan

2,555 units - Rukan, Dubailand

1,499 units

Leading five Dubai submarkets – Future property supply (2025-2027)

- Jumeirah Village Circle

24,990 units - Business Bay

16,009 units - Azizi Venice

13,458 units - DAMAC Lagoons

11,117 units - Arjan

8,976 units

DPI Property Price Trend

Source: Property Monitor

2024 Sales by Property Type | Residential

Source: Property Monitor

By property type, apartments dominated the market, accounting for 81% of total sales, while townhouses comprised 13% and villas made up the remaining 6%.

Construction Status

Source: Property Monitor

With the surge in new project launches, 68% of residential properties in Dubai are currently under construction— the highest percentage in recent years.

New Project Launches in 2024 | Top Developers

Source: Property Monitor

Emaar Properties, Binghatti Properties, and DAMAC Properties led the market in new launches, ranking highest in both units released and total sales value.

Rental Yields & Payment Preferences

Dubai’s apartment gross rental yields remain strong, offering returns for property investors across a variety of key areas that surpass other comparable international markets. As of December 2024, Dubai Investments Park was leading the way with an impressive 10.3% yield, followed closely by International City at 9.4%. The average apartment rental yield in Dubai for December 2024 stood at 7.4% while villas/townhouses had a rental yield of 5.1%.

This evidence shows that rental yields continue to make Dubai an attractive destination for investors seeking strong returns.

Top 10 Residential Areas in Dubai with the Highest Gross Rental Yields (as of Dec 2024)

| Areas | Gross Rental Yield |

|---|---|

| Dubai Investments Park | 10.3% |

| International City | 9.4% |

| Dubai Production City | 8.6% |

| Downtown Jebel Ali | 8.6% |

| Liwan | 8.5% |

| Dubai Silicon Oasis | 8.4% |

| Discovery Gardens | 8.3% |

| Arjan | 8.3% |

| Dubai Residence Complex | 8.2% |

| Dubai Sports City | 8.2% |

Source: Property Monitor

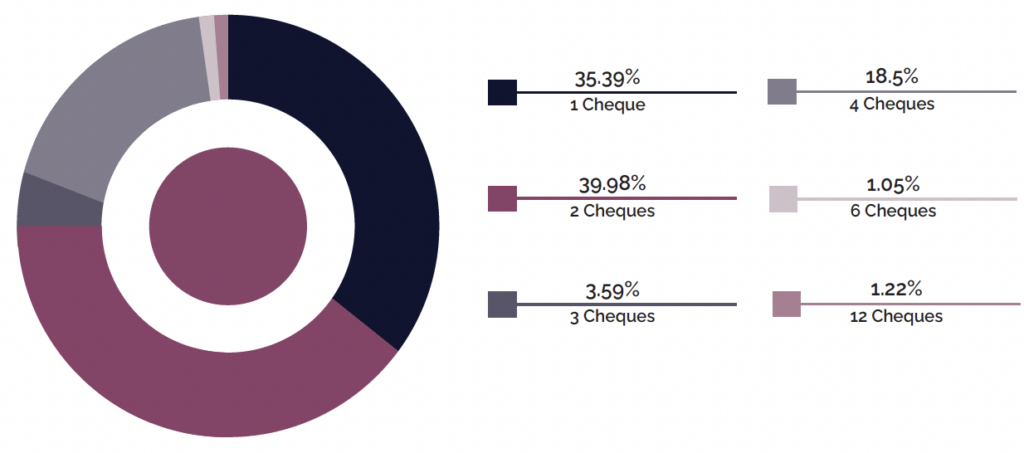

In addition to strong rental yields, payment preferences also play a key role in market dynamics. The graph below highlights the distribution of residential rent payment cheques in Dubai from January to December 2024. There is a clear preference for fewer cheques.

Most tenants either pay by two cheques (39.98%) or by a single cheque (35.39%), while 18.5% opt for four cheques. Other payment structures, including three, five, six, eight, nine, and twelve cheques, are far less common. This trend reflects landlords’ preference for lump-sum payments, with tenants generally adapting to these terms. Rental rates often vary based on the number of cheques, with fewer payments typically resulting in lower rental rates.

Rent Cheque Trends – FY 2024

Source: Property Monitor, Cavendish Maxwell Research

Monitoring the Property Pipeline

Property Monitor tracks not only transactions but also the precursors to these sales. Prior to a sale being recorded, the platform monitors the mortgage process and property evaluations. It also tracks contracts, sales and buy agreements (SBAs), and listings. This comprehensive data provides valuable insights into the market pipeline at various stages. Indicators suggest that recent milestones represented the peak of the current market cycle, where we saw over 20,000 transactions recorded in a single month in October. The steady pipeline of off-plan projects, combined with ongoing demand for ready properties, indicates that the gap in transactions volumes between the ready market and the off-plan market may continue to widen in the coming months.

2025 Real Estate Market Outlook

Looking ahead, 2025 will be a defining year for Dubai’s real estate sector. With off-plan development continuing at historic levels, investor interest holding firm, and government-backed initiatives such as the Dubai Economic Agenda (D33) and the Real Estate Sector Strategy 2033 providing long-term confidence, Dubai remains well-positioned for continued growth. However, as the market matures, expectations must adjust to a more balanced trajectory—one that favours sustainability over rapid expansion. While the big gains of the past four years may be behind us, stability, liquidity, and strategic development will be the key themes shaping the year ahead.