UAE: Did you know that ‘yields’ and ‘returns’ (ROI) have slightly different meanings when investing in real estate? Let’s find out!

Dubai: Smart investors understand that investing in real estate is the best way to make a good passive income. It’s a great medium to put your money to work, making financial gains.

Investing in the property market in the UAE, in particular, is considered a lucrative investment destination, as the place generates high rental yields when compared to several other property investment havens worldwide.

“Dubai’s emerging and budget freehold areas offer higher yields of nearly 9 per cent, followed by midmarket neighbourhoods,” said Vijay Valecha, chief investment officer at Dubai-based investment brokerage Century Financial. “Whereas Abu Dhabi’s yields averaged at 7.4 per cent, with apartment returns at 7.7 per cent and villas 6.9 per cent.”

Although these figures look attractive, an informed investor must understand what a property deal is worth for them when taking a plunge into the real estate market.

Know that not all property deals are a good investment.

Evaluating the profit figure carefully to figure out whether the property will make good financial gains or yields for you becomes a vital part of property investment.

Understand what yields are being talked about to make prudent investments.

You must check whether developers, brokers, marketers, property advertisements, and the real estate consultancy reports highlight the gross yields, net yields, and total returns on investment (ROI) to determine the property’s real worth.

So, what is gross yield, net yield and total return on investment (ROI)?

Gross yield, net yield and total return on investment (ROI) are three simple performance metrics used to assess the property on a non-time adjusted basis, explained Zhann Jochinke, chief operating officer (COO) at Dubai-based market analytics firm Property Monitor.

Gross yield (GY) is the income of the property divided by its purchase price. “This is often seen on the property portals or referenced in marketing material, which is often stated as ‘yield’, and that can be misleading. It does not take into account operating expenses, debt service or acquisition costs,” Jochinke said.

Gross Yield is the income return on an investment before expenses are deducted.

Formula: Gross Yield = Annual Rent / Purchase Price

Net yield (NY) is the income on the property after expenses. “It is more reliable as it takes account of the operating expenses and ‘debt service’ (explained below). Some of the main operating expenses are services charges, insurance, allowances for repairs and maintenance, and potentially, professional property management fees. Net yield provides a more accurate guide than gross yield as it’s based on the actual amount of money (cash flow) you will end up with after costs,” he added.

Net yield is the income return on an investment after expenses have been deducted.

Formula: Net Yield = (Annual Rent – (Operating Expense + Debt Service) / Purchase Price

ROI provides a more accurate assessment as the annual profits after expenses are divided by the cash put in. “Like net yield, it takes into account operating expenses and debt service to give a cash flow. However, instead of dividing by the purchase price, it goes a step further by looking at the amount of cash you have invested in acquiring the property,” he said.

“Depending on the amount, rate, and type of leverage (mortgage or debt) availed, it can greatly modify the return. Therefore, ROI stands out and becomes a beneficial way to assess investment and get an accurate measure of how hard your cash will be working.”

ROI is the total return on an investment property.

Formula: ROI = Annual Return (Annual Cash Flow) / Total Investment (Acquisition Costs)

Here is an illustration with calculation to make GY, NY and ROI easier to understand.

For example, let’s say Mr. XYZ and Mr. ABC purchased a studio apartment each in Cayan Tower, Dubai Marina, as an investment property, priced at Dh1 million. It’s a 767 square feet (sqft), unfurnished unit, with service charges of Dh 14.3 per sqft. The market annual rent (income) on the unit is Dh60,000.

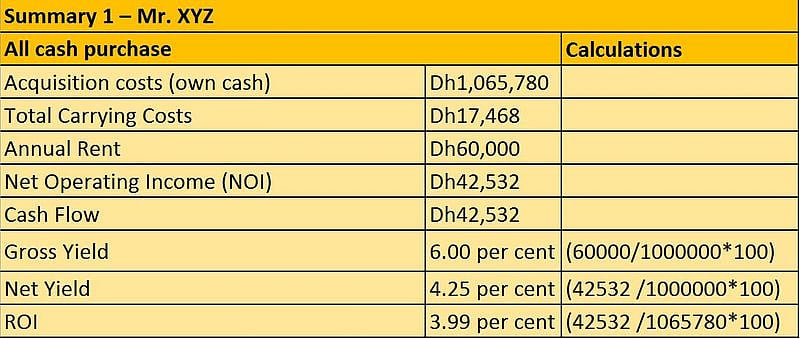

Mr. XYZ has purchased the property on all cash:

• Acquisition costs

His acquisition cost of purchasing the unit is (Dh1,000,000) plus the transactions fees of buying a property in Dubai. Transactions fees include broker fees 2 per cent of the property value plus VAT 5 per cent on the fee (Dh21,000), Dubai Land Department (DLD) transfer fees 4 per cent plus fixed cost of Dh580 (Dh40,580) and a fixed registration trustee fee of Dh4,000 plus VAT 5 per cent on the fee (Dh4,200). So, his total transaction cost is (Dh65,780).

In this case, the total acquisition costs (own cash) is Dh1,000,000 + Dh65,780, that is Dh1,065,780.

• Annual operating expenses

His annual operating expenses on cash purchase include service charges, i.e., size of the unit multiplied by service charge rate, which in this illustration: (767×14.3) = Dh10,968, plus other expenses. These are insurance costs (Dh 1,500), maintenance and repairs (Dh 2,000) and a 5 per cent property management fee (Dh 3,000).

His total annual operating expenses is Dh10,968 + Dh1,500 + Dh2,000 + Dh3,000, that is Dh17,468.

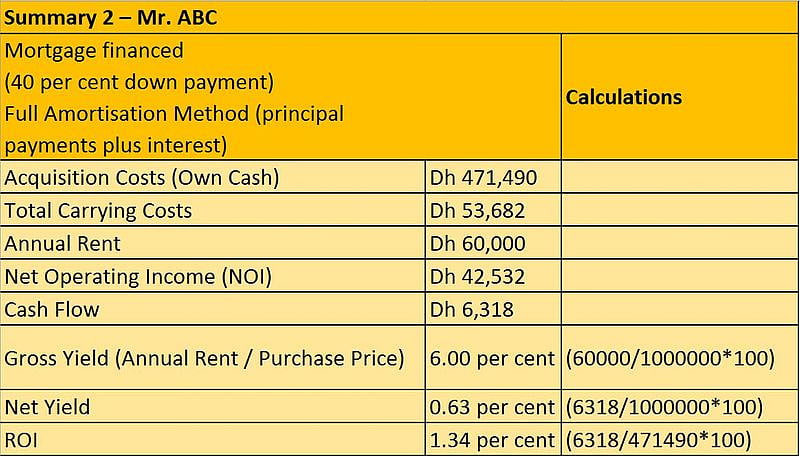

Mr. ABC purchased the same unit using bank finance:

The property costs Dh1,000,000; he took a bank mortgage, paid a down payment of 40 per cent of the property value (Dh400,000), so his principal amount of loan is 60 per cent (Dh600,000). The loan tenure of 25 years – fixed-rate for 3 years, and the mortgage interest rate of 2.75 per cent. The monthly mortgage payment is (D 2,768), calculated using PMT is a built-in function in Excel, and the interest only portion of the payment is (Dh1,375)

• Acquisition costs

His acquisition cost of purchasing the unit is (Dh400,000) plus the transactions fees of buying a financed property in Dubai. These charges include broker fees 2 per cent of the property values plus VAT 5 per cent on the fee (Dh21,000), DLD transfer fees 4 per cent plus fixed cost of Dh580 (Dh40,580) and a fixed registration trustee fee of Dh4,000 plus VAT 5 per cent on the fee (Dh4,200), similar to what is paid by cash buyers.

The additional costs on mortgage purchases include a fixed mortgage valuation fee of Dh2,500 plus VAT 5 per cent on fee (Dh2,625). Then mortgage arrangement fee is 0.25 per cent of the financed amount of Dh600,000, which is Dh1,500 plus VAT 5 per cent on fee (Dh1,575) and mortgage registration fee 0.25 per cent of the financed amount of Dh600,000, which is Dh1,500 plus Dh10 (Dh1,510). So his total transaction cost is (Dh71,490).

His total acquisition cost (own cash) is Dh400,000 + Dh71,490 is Dh471,490.

• Annual financing costs

His annual financing costs in the full amortisation mortgage payment method (principal payments plus interest, explained below) are Dh33,214 plus life insurance premium paid 0.50 per cent of the financed amount of Dh600,000, that is Dh3,000, which equals to Dh36,214.

In the interest-only mortgage payment method (explained below), it is Dh16,500 plus life insurance premium 0.50 per cent of the financed amount of Dh600,000, which is Dh3,000, which equals to Dh19,500.

• Annual operating expenses

His total annual operating expenses is same as of Mr. XYZ ‘s cash purchase that is Dh10,968 + Dh1,500 + Dh2,000 + Dh3,000 = Dh17,468.

Jochinke explained that in the case of mortgage options, the costs are higher because you have mortgage payments to account for, and therefore the profit is lower.

“By using leverage (explained below) through mortgage financing, you end up with a higher ROI than net yield because you are putting in much less cash. The interest-only loan can greatly increase the ROI.”

• Annual operating expenses

His total annual operating expenses is same as of Mr. XYZ ‘s cash purchase that is Dh10,968 + Dh1,500 + Dh2,000 + Dh3,000 = Dh17,468.

Jochinke explained that in the case of mortgage options, the costs are higher because you have mortgage payments to account for, and therefore the profit is lower.

“By using leverage (explained below) through mortgage financing, you end up with a higher ROI than net yield because you are putting in much less cash. The interest-only loan can greatly increase the ROI.”

This article was originally published in Gulf News.